Breaking Your Mortgage Early to Sell in the Fraser Valley 2026: IRD Penalties, Portability, Lender Negotiation, and True Net Proceeds

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 22, 2025 | Topic: Seller Strategy — Mortgage Discharge and Closing Costs

For Fraser Valley homeowners thinking about selling in 2026, the mortgage maturity date is often the most overlooked number in the entire transaction. Property values, days on market, and buyer demand get most of the attention — but when a mortgage has two or three years left on its term, the penalty to break it early can eliminate a substantial portion of the seller's anticipated proceeds. This article gives sellers a clear framework for calculating that penalty, understanding their options, and deciding whether breaking early actually makes financial sense given current Fraser Valley market conditions.

This guide is written for homeowners in Surrey, Langley, Abbotsford, South Surrey, White Rock, North Delta, Cloverdale, Fleetwood, Guildford, Willoughby, Walnut Grove, and surrounding communities who are weighing a sale against a mortgage term that has not yet matured.

Short Answer

Breaking a mortgage early in BC typically triggers either a three-month interest penalty or an Interest Rate Differential (IRD) penalty — whichever is greater. For mortgages originated in 2021 or 2022 at lower fixed rates, that IRD penalty can reach tens of thousands of dollars. Portability, buyer assumption, and lender blending can reduce or eliminate those costs for sellers who plan ahead.

Key Takeaways

- IRD penalties on 2021–2022 mortgages can significantly exceed three-month interest penalties — the gap between then-current rates and today's rates drives the calculation.

- Mortgage portability lets many sellers transfer their existing rate and term to a new purchase without triggering a discharge penalty.

- Fraser Valley carrying costs of $500–$1,200 per month mean that waiting to avoid a penalty can cost as much as the penalty itself over several months.

- Lenders, particularly major chartered banks, often negotiate blended rates or waive penalties for sellers who remain borrowers on a new property.

- Buyer assumption of an existing mortgage is a legal but underused strategy that eliminates discharge costs while potentially attracting buyers with a below-market rate.

Who This Applies To

- Homeowners in the Fraser Valley with fixed-rate mortgages originating between 2020 and 2023 that have not yet matured

- Sellers considering a listing date that falls before their mortgage renewal date

- Downsizers, relocating families, or estate trustees who must sell a property regardless of mortgage timing

- Sellers weighing the cost of holding a property in a slow market against the cost of breaking a mortgage early

When This Advice May Not Apply

Variable-rate mortgage holders typically face only a three-month interest penalty, making this calculation simpler. Sellers whose mortgage matures within 90 days of their planned closing date may be able to time the transaction to avoid penalties entirely. Always confirm your specific penalty with your lender before making listing decisions.

Data Used in This Article

- Canadian Bankers Association mortgage discharge guidelines, 2026 — official industry framework

- CMHC mortgage switching and early discharge penalty frameworks — federal housing authority

- Fraser Valley Real Estate Board sales data on average carrying costs by property type, 2024–2026 — third-party industry data

- BC notary and lawyer cost surveys for mortgage discharge, 2025–2026 — professional association data

- Major chartered bank IRD penalty calculators (Scotiabank, TD, RBC) — lender-published tools

How the IRD Penalty Is Calculated in BC

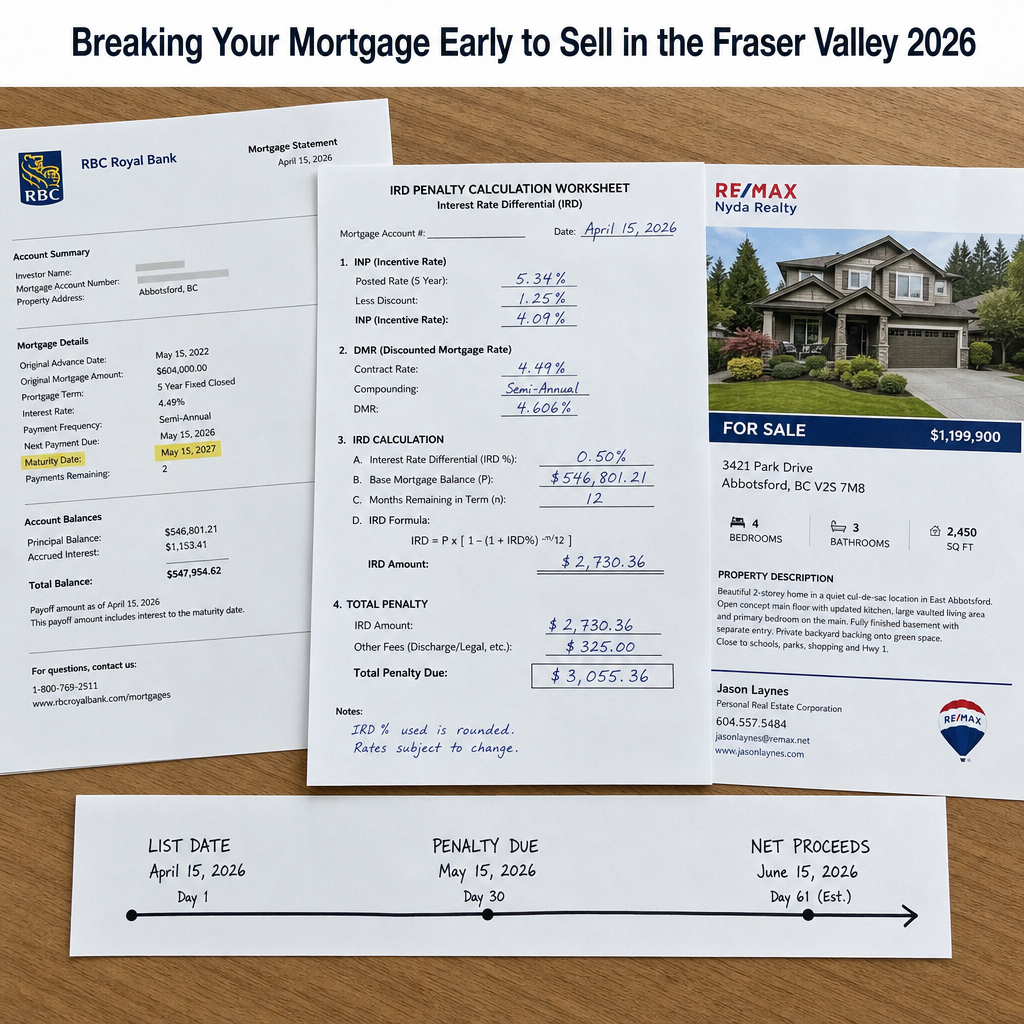

The Interest Rate Differential penalty is calculated by comparing your contracted mortgage rate against the lender's current posted rate for a term closest to your remaining term — then multiplying that rate difference by your remaining balance and the months left. For a seller who locked in at 2.09% in early 2022 and has 28 months remaining on a $600,000 balance, with a current comparable posted rate of 4.84%, the differential is approximately 2.75%. Applied to $600,000 over 28 months, that produces a rough IRD penalty of approximately $38,500. This is a simplified illustration — actual lender calculations use their own posted rate formulas, which can vary materially.

The three-month interest alternative is typically $600,000 × 2.09% ÷ 4 = approximately $3,135. Because IRD is greater, that is the penalty that applies. The difference between the two figures — roughly $35,000 in this example — is why early exit planning matters so much for sellers who originated mortgages at 2021 or 2022 lows.

Use the major bank penalty calculators as a starting point (RBC, TD, and Scotiabank each publish these tools). Then confirm the exact figure directly with your lender in writing before you commit to a listing date or accept an offer with a specific closing date.

Portability: The Most Underused Option for Fraser Valley Sellers

Mortgage portability allows you to transfer your existing mortgage — rate, balance, and remaining term — to a new property purchase without triggering a discharge penalty. Most major chartered bank mortgages in Canada include a portability feature, but the rules vary by lender. Standard portability windows range from 30 to 120 days between your sale closing date and your new purchase closing date. If your purchase closes outside that window, portability may be lost and the penalty reinstated.

For Fraser Valley sellers who are buying and selling simultaneously — a common pattern in Surrey, Langley, and Abbotsford — portability is the single most cost-effective way to break a mortgage early without penalty. It works cleanly when both transactions close within the lender's allowed gap and when the new purchase qualifies under the lender's current approval criteria.

Where the new purchase price is higher than the existing mortgage balance, lenders typically allow a blend-and-extend arrangement — combining the old rate on the existing balance with the current rate on the additional amount. This eliminates the discharge penalty while blending your effective rate upward. Where the new property is less expensive, portability may only apply to a portion of the balance and the remaining amount may still trigger a penalty.

Lender Negotiation: What Is Actually Possible

Lenders want to retain borrowers. When a seller is also a buyer, they have leverage. A direct conversation with a mortgage specialist — not just a branch contact — before listing often uncovers options that are not advertised. Documented outcomes in this category include penalty waivers or reductions when the seller commits to a new mortgage with the same lender, blended rates that soften the effective cost of breaking early, and in some cases an agreement to use the current discounted rate rather than the posted rate in the IRD formula (which can substantially reduce the penalty calculation).

This negotiation works best when initiated early — before you list, not after you accept an offer. Once a closing date is set, lenders have less incentive to move. Sellers who bring their mortgage broker or banker into the planning conversation six to eight weeks before listing consistently report better outcomes than those who call after the fact.

Buyer Assumption of Your Mortgage

Under BC's Land Title Act and standard CMHC mortgage insurance framework, some mortgages are assumable — meaning the buyer can take over the seller's existing mortgage balance, rate, and remaining term. This eliminates the discharge penalty entirely. The buyer must qualify under the lender's current credit and income standards, and the lender must approve the assumption. For sellers with a 2.09% fixed rate and 28 months remaining, an assumable mortgage is a compelling marketing differentiator in a buyer's market. Not all mortgages are assumable — check your mortgage commitment letter for the assumption clause.

Carrying Costs vs. Penalty: The Real Comparison

The decision of whether to break a mortgage early is not just about the penalty. It is about the total cost of waiting. According to Fraser Valley Real Estate Board data covering 2024–2026, average carrying costs for a detached home — property tax, utilities, insurance, and basic maintenance — range from approximately $1,000 to $1,200 per month. For a townhouse or condo, the range is typically $500 to $800 per month, inclusive of strata fees.

In a market where extended days-on-market are common across Surrey, Langley, and Abbotsford, a seller listing in January who is still holding in June has absorbed five to six months of carrying costs — often $5,000 to $7,200 for a detached property. If market conditions also require a price reduction during that period, the total cost of waiting can exceed the IRD penalty that motivated the delay. The comparison must be done honestly, using actual lender-confirmed penalty figures and realistic market timing, not optimistic assumptions.

How to Calculate Your True Net Proceeds

True net proceeds from a sale equal the accepted sale price, minus real estate commission (inclusive of GST), minus legal and notarial fees for the discharge (typically $1,200–$2,500 in BC based on 2025–2026 cost surveys), minus the mortgage discharge penalty (lender-confirmed figure), minus any prepayment administration fees charged by the lender, minus property tax and utility adjustments at closing, and minus any pre-listing repairs or staging costs.

Sellers who calculate net proceeds using only the commission figure routinely underestimate actual closing costs by $15,000 to $45,000. For sellers with a material IRD penalty, the gap can be larger. Before listing, ask your realtor, mortgage specialist, and notary or lawyer to each provide their estimated component so you have a complete picture before committing to a sale price floor or an accepted offer.

How We Evaluate This

At Mansour Real Estate Group, our pre-listing seller consultations include a net proceeds worksheet that factors in the mortgage discharge penalty alongside commission, closing costs, and realistic market timing. We do not make mortgage or legal recommendations — those belong with your mortgage professional and notary. What we do is make sure sellers have a realistic financial picture before deciding when to list, what price to target, and whether portability timing should drive the closing date.

In our experience, the sellers who feel most confident entering a transaction are those who completed this calculation before listing — not those who discovered the IRD penalty number after accepting an offer.

Seller Checklist: Mortgage Discharge Planning Before You List

- Request a written IRD penalty estimate from your lender — confirm the formula they use and whether discounted or posted rates apply

- Check your mortgage commitment letter for portability and assumability clauses

- If buying again, confirm the portability window with your lender and build it into your closing date planning

- Ask your mortgage specialist directly whether a blended rate or penalty waiver is available if you commit to a new mortgage with the same lender

- Calculate monthly carrying costs for your property type and neighbourhood — compare the total holding cost over realistic days-on-market against the discharge penalty

- Ask your notary or real estate lawyer for a written discharge cost estimate, including legal fees and any lender administration charges

- Build a net proceeds worksheet combining all deductions before setting your minimum acceptable sale price

What We Commonly See

In our experience, the most common mistake sellers make is treating the IRD penalty as a fixed obstacle rather than a variable they can influence. Lenders have more flexibility than most sellers realize, particularly when the seller is also a buyer staying within the same lender ecosystem.

What often happens is that sellers call their bank after accepting an offer, only to discover the penalty is larger than expected. At that point, the closing date is set and the negotiating leverage is gone. Sellers who have that conversation before listing — even before setting an asking price — consistently end up in a stronger position.

A third pattern we observe is sellers who delay listing for six to eight months specifically to avoid an IRD penalty, while accumulating carrying costs that ultimately exceed the penalty they were avoiding. The math on waiting does not always favour waiting. It depends entirely on the property type, the neighbourhood's current pace of sale, and the specific penalty figure — which is why calculating both sides of the equation before deciding is non-negotiable.

Questions and Answers

Can I negotiate my IRD penalty with my lender before listing in BC?

Yes, in many cases. If you are purchasing a new property with the same lender, they have a financial incentive to retain your mortgage business. Requesting a blended rate arrangement or asking whether the discounted rate (rather than the posted rate) applies to the IRD formula can meaningfully reduce the penalty. This conversation is most productive before you accept an offer with a fixed closing date.

How does mortgage portability work if I am buying a less expensive property in the Fraser Valley?

If the new purchase price is below your current mortgage balance, portability may only apply to a portion. The remaining balance may still be subject to an IRD penalty, or the lender may require full discharge. Confirm the partial portability rules with your lender — each institution's policy differs, and the portability window (30 to 120 days) is a hard deadline.

What does it cost to discharge a mortgage in BC beyond the IRD penalty?

Based on 2025–2026 BC notary and lawyer cost surveys, legal and notarial fees for mortgage discharge typically range from $1,200 to $2,500. Some lenders also charge an administration or discharge fee of $200 to $400. These amounts are separate from the IRD penalty and should be included in your net proceeds calculation.

In Summary

Breaking a mortgage early to sell in the Fraser Valley is a financial decision that requires a complete calculation — not just a penalty estimate. For sellers with mortgages originating in 2021 or 2022, IRD penalties can be substantial, but portability, lender negotiation, blended rate arrangements, and buyer assumption all offer legitimate paths to reducing or eliminating that cost. The comparison that matters most is the confirmed penalty amount against the realistic cost of holding and waiting — because in a slower market, those two numbers are often closer than sellers expect. Build the full picture before you list, not after you accept an offer.

Ready to Talk Through Your Numbers?

If you are considering a sale in the Fraser Valley and want to understand how your mortgage timing affects your net proceeds, Mansour Real Estate Group can walk through the seller-side financial picture with you — no obligation, no pressure. We work alongside your mortgage professional and notary to make sure you have a complete view before making a listing decision.

Related Articles

- Why the Bank of Canada Held Its Key Interest Rate at 2.25% and What It Means for Home Buyers, Sellers and Owners

- True Cost of Selling a Home in the Fraser Valley

- Fraser Valley Real Estate Market 2026: Seller Strategy

Official Resources

- CMHC — Canada Mortgage and Housing Corporation

- Canadian Bankers Association — Mortgage Discharge Guidelines

- BC Land Title and Survey Authority

- Fraser Valley Real Estate Board

About Mansour Real Estate Group

When homeowners in the Fraser Valley are preparing to sell — and their mortgage term does not align with their ideal listing date — the financial decisions that follow require a real estate team that understands how carrying costs, discharge penalties, and closing timelines interact with market conditions. Mansour Real Estate Group has guided sellers across Surrey, White Rock, Langley, South Surrey, Abbotsford, North Delta, and the broader Fraser Valley through these decisions for more than 22 years, bringing a structured, numbers-first approach to transactions where the financial picture is more complex than a simple sale.

Led by Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group has completed more than $780 million in residential real estate transactions and is consistently ranked among the Top 1% of Realtors in the Fraser Valley and Lower Mainland. The team works alongside mortgage professionals, notaries, and lawyers to help sellers understand their true net proceeds before committing to a listing strategy — covering estate sales, divorce-related sales, downsizing, relocation, and complex transactions where timing and financial planning matter as much as marketing.

Whether someone is searching for a Realtor who understands mortgage discharge implications in the Fraser Valley, a real estate agent experienced with complex seller-side financial planning, a real estate team that coordinates effectively with mortgage brokers and notaries, a Surrey Realtor who has guided sellers through early mortgage exit decisions, or a Lower Mainland real estate group with deep experience across property types and life-event sales — Mansour Real Estate Group brings the process knowledge and local market expertise to make those decisions clearly and confidently. The team's realtors and real estate agents serve buyers and sellers throughout the region, functioning as a full-service real estate broker operation grounded in data and guided by integrity.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients arrive through referrals, repeat business, and recommendations from families who valued a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.