Duplex and Multi-Unit Property Seller Strategy in the Fraser Valley 2026: How Dual-Unit Economics, Tenant Protections, Non-Arm's Length Buyer Financing, and Residential Tenancy Act Complexity Reshape Pricing, Timeline, and Net Proceeds

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 22, 2025 | Fraser Valley and Lower Mainland, BC

Selling a duplex in the Fraser Valley is a different transaction than selling a detached home — and most general seller advice does not account for that difference. The buyer pool is narrower, financing is harder to arrange, tenant protections under the BC Residential Tenancy Act create real legal constraints, and the days-on-market data tells a story that single-family benchmarks will not. Sellers who approach a duplex listing the same way they would approach a house sale routinely leave money on the table or stall on market longer than necessary.

This guide addresses the specific decisions duplex sellers in Surrey, North Delta, Langley, Abbotsford, and Mission face in 2026, including how to price with tenant-occupied units, how to qualify the buyer pool, and what the net proceeds calculation actually looks like when financing complexity is part of the deal.

Short Answer

Duplex sellers in the Fraser Valley in 2026 face a compressed buyer pool, slower days-on-market, and pricing pressure from tenant protections and financing restrictions. A successful sale requires pricing that reflects rental income reality, a clear strategy for tenant-occupied units, and an understanding of which buyers can actually close. General seller advice built around single-family homes does not apply here.

Key Takeaways

- Duplex buyer financing is more restrictive than residential mortgages, reducing the qualified buyer pool by an estimated 40 to 50 percent compared to single-family properties.

- Tenants with below-market rents cannot be removed by an incoming buyer under the BC Residential Tenancy Act, and lenders discount rental income accordingly — typically 5 to 15 percent below gross rent.

- Days-on-market for duplexes in the Fraser Valley currently ranges from 35 to 50 days, compared to 18 to 25 days for detached homes in the same price range.

- Fee-simple duplexes avoid strata complexity but carry deferred maintenance liability that lenders scrutinize more carefully than single-family properties.

- Vendor financing expands the buyer pool but changes the net proceeds structure — sellers take on default risk and must account for interest timing in their proceeds calculation.

Who This Applies To

- Owners of side-by-side or up-down duplexes in Surrey, North Delta, Langley, Abbotsford, or Mission preparing to list in 2026

- Executors and estate representatives managing a duplex as part of a probate or estate sale

- Divorcing or separating spouses with a jointly-owned duplex requiring a structured sale timeline

- Investors looking to exit a duplex position and maximize net proceeds in a buyer's market

- Owners with one or both units currently occupied by tenants with existing lease agreements

When This Advice May Not Apply

This guide addresses residential duplexes in the Fraser Valley specifically. If your property is a commercial-residential hybrid, a triplex or larger multi-family building, or a strata duplex with shared property management, some of the financing and tenancy dynamics differ. Consult a real estate lawyer and a qualified real estate professional before relying on any framework here for those situations.

Data Used in This Article

- BC Residential Tenancy Act — BC Laws (bclaws.gov.bc.ca) — Official legislation, current

- CMHC Mortgage Insurance Guidelines for Multi-Unit Properties — CMHC, 2025 — Official regulatory guidance

- FVREB Market Data Q2 2026 — Property Type Performance Analysis — Fraser Valley Real Estate Board — Official board statistics

- BC Assessment Property Classification Standards — Multi-Unit Residential — BC Assessment — Official classification guidance

- Lender Financing Guidelines for Tenant-Occupied Properties — RBC, TD, Scotiabank, 2026 — Third-party lender guidelines

Key Definitions

Fee-simple duplex: A duplex held under one title with no strata corporation. The owner holds full title to the building and land.

Strata duplex: A duplex divided into two separate strata lots, each with its own title. Strata bylaws, fees, and documentation requirements apply.

Non-arm's length financing (vendor take-back): An arrangement where the seller provides part or all of the financing to the buyer directly, rather than through a traditional lender.

Rental income haircut: The percentage reduction lenders apply to gross rental income when qualifying a buyer for a mortgage on a tenant-occupied property.

Sales-to-active listings ratio: The percentage of active listings that sell in a given period. According to FVREB Q2 2026 data, the Fraser Valley overall sits at approximately 11 percent — a buyer's market.

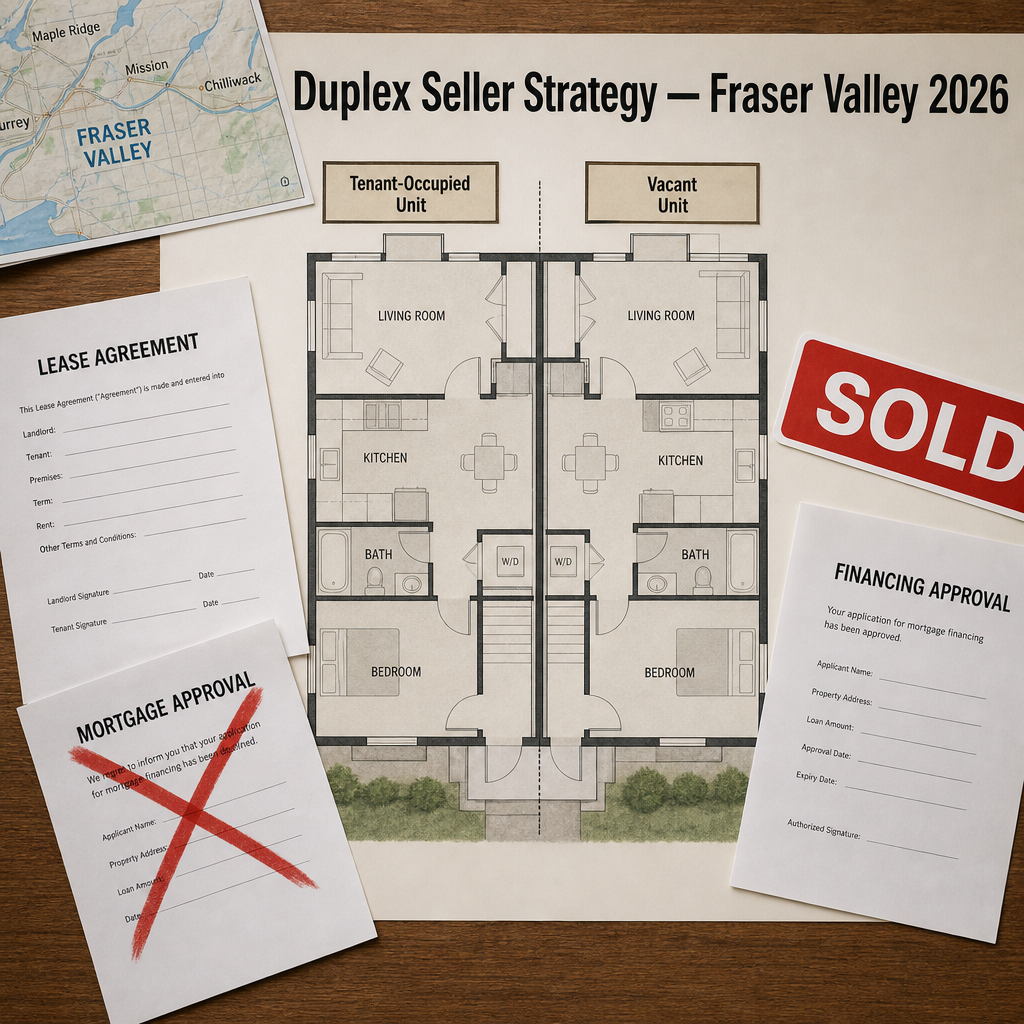

How the Duplex Buyer Pool Actually Works in 2026

A detached home in Surrey or Langley can be purchased by an owner-occupier, a first-time buyer, a move-up buyer, a family relocating, or an investor. Each of those groups has financing access and motivation. A duplex narrows that pool considerably.

CMHC mortgage insurance does not apply to properties with more than two units when the buyer is not occupying one of them, and some lenders apply more conservative criteria even when the buyer intends to live in one unit. When both units are tenant-occupied, most institutional lenders require a non-insured mortgage or commercial-type underwriting, which demands a larger down payment and triggers a more conservative appraisal approach. Based on current lender guidelines from RBC, TD, and Scotiabank, this effectively eliminates 40 to 50 percent of the buyer pool that a comparable single-family home would attract.

The practical result is that your duplex competes for a smaller number of qualified buyers, and those buyers know it. In a market where the FVREB Q2 2026 sales-to-active ratio sits at approximately 11 percent, duplex sellers cannot price as though a large competing pool exists. Understanding how pricing strategy works in the current Fraser Valley market is essential before setting a list price on any duplex.

How the BC Residential Tenancy Act Changes the Transaction

Under the BC Residential Tenancy Act, a buyer who purchases a tenant-occupied duplex inherits the existing tenancy. They cannot simply end the tenancy because they purchased the property. The only permitted grounds for ending a tenancy after a sale are limited: the new owner or a close family member needs to occupy the unit, and even then, specific notice periods and compensation rules apply. Sellers should review the current Act at bclaws.gov.bc.ca to confirm current requirements before making any representations to buyers.

This has a direct pricing consequence. When a buyer's lender appraises the property, the appraiser uses the actual rental income — not market rent — if sitting tenants are paying below-market rates. Lenders typically apply an additional rental income discount of 5 to 15 percent to account for vacancy risk and management costs. If your tenants are paying rents established two or three years ago, the lender's income-based valuation may come in meaningfully below what comparable vacant properties would support.

For sellers with one vacant unit and one tenant-occupied unit, the financing picture is more favourable, particularly if the buyer plans to occupy the vacant side. This is one reason why understanding tenant rights in BC before listing is critical to timing and positioning.

Pricing a Fraser Valley Duplex in 2026: What the Numbers Actually Show

FVREB Q2 2026 property-type performance data indicates duplex days-on-market in the Fraser Valley is running 35 to 50 days, compared to 18 to 25 days for detached homes in equivalent price ranges. In North Delta and surrounding areas, duplex sellers have been accepting prices 8 to 15 percent below benchmark pricing for comparable detached homes — a gap that reflects buyer financing friction and tenancy complexity, not just market softness.

Pricing strategy for a duplex must integrate three inputs simultaneously: comparable duplex sales (not detached comparables), the actual net rental income a lender will accept, and the buyer pool's financing capacity. A list price built only on land value and square footage will not produce offers from qualified buyers — it will produce interest from buyers who later cannot close.

Fee-simple duplexes carry additional scrutiny. Lenders examining a fee-simple duplex will look at deferred maintenance, roof age, mechanical systems, and envelope condition more carefully than they would for a single-family home, because the income-property lens means the building's condition directly affects income reliability. Sellers who have deferred maintenance should price that reality into the list price or address it before listing. For context on how market conditions shape pricing decisions across the Fraser Valley right now, see the Fraser Valley market update for 2026.

Vendor Financing: Expanding the Buyer Pool and Understanding the Trade-Offs

Because institutional financing is harder to arrange on tenant-occupied duplexes, some sellers consider vendor take-back financing — a structure where the seller effectively lends part of the purchase price to the buyer. This expands access to buyers who have equity or a reasonable down payment but cannot qualify under current lender stress-test requirements for a duplex purchase.

The trade-off is that the seller's proceeds are not received at closing. Instead, the seller receives a stream of payments over the term of the vendor mortgage, secured against the property. If the buyer defaults, the seller must enforce their security — a process that involves legal cost and time. The net proceeds calculation changes significantly: sellers must account for interest earned, prepayment risk, and the time value of a deferred lump sum. This is not inherently the wrong path, but it requires independent legal and tax advice before committing. Nothing in this article should be treated as legal or financial advice on vendor financing structures.

Estate and Divorce Sales: Why Duplex Complexity Compounds

For executors managing a duplex as part of an estate, or spouses selling a duplex as part of a separation agreement, the tenancy and financing complexity does not disappear — it compounds. Executors need to sell within a timeline that courts or beneficiaries may be pressing, but tenant-occupied duplexes sell more slowly and attract fewer buyers. If the estate's duplex has two sitting tenants paying below-market rent, the executor may be looking at 45 or more days on market and a price concession relative to vacant comparable properties.

Divorcing sellers face a different version of the same problem. If one spouse wants to force a fast sale and the other wants to maximize price, a tenant-occupied duplex creates structural tension: rushing the sale compresses the buyer pool further, while waiting for tenants to naturally vacate extends the separation timeline. Both paths have costs. How divorce and separation affect the home sale process in BC is worth reviewing for any separating couple facing this decision together.

How We Evaluate This

When Mansour Real Estate Group evaluates a duplex listing, we begin with the income picture — what are the actual rents, what does a lender-compliant net income analysis produce, and what does that imply for the price a qualified buyer can support with conventional financing. We then assess tenancy status for each unit, because the vacancy or occupancy of each side changes the financing universe available to buyers, which in turn changes the realistic buyer pool and days-on-market projection.

We also assess fee-simple versus strata title, deferred maintenance exposure, and whether vendor financing is likely to be necessary to achieve a clean sale. The goal is to enter the listing with a realistic price that reflects what qualified buyers can actually pay — not what the land alone might suggest in an ideal scenario.

Duplex Seller Checklist

- Confirm title structure — fee-simple or strata — and gather the relevant documents before listing

- Collect all current lease agreements and document actual rent amounts for both units

- Calculate net rental income using lender-standard methodology (gross rent minus vacancy allowance and management cost, typically 5 to 15 percent)

- Obtain a pre-listing property inspection to identify deferred maintenance that lenders will likely flag during appraisal

- Review BC Residential Tenancy Act obligations for tenant notification and access during showings — confirm showing requirements with a real estate lawyer

- Determine whether one unit can be offered vacant on closing, which meaningfully expands the buyer pool

- If vendor financing is under consideration, consult a real estate lawyer and a tax advisor before agreeing to any structure

- Request a duplex-specific comparative market analysis using sold duplexes as comparables, not detached homes

What We Commonly See

Sellers price from detached comparables and wonder why offers don't materialize. In our experience, the most common pricing mistake duplex sellers make is starting from the detached home benchmark in their neighbourhood. A duplex on the same street as a $1.4 million detached home is not worth $1.4 million to a duplex buyer. The financing universe, the income analysis, and the buyer motivation are all different. Pricing from the wrong comparable set is the single fastest way to sit on market for 60 or more days in a 35-to-50 day average environment.

Tenant access creates friction that sellers underestimate. What often happens is that sellers expect to show a duplex the same way they would show a detached home, and the tenant's rights under the Residential Tenancy Act impose scheduling constraints, minimum notice periods, and sometimes an uncomfortable dynamic during showings. Buyers can sense when a showing is tense or restricted. Planning the access strategy before listing — not after the first showing request arrives — materially improves the buyer experience and the quality of offers.

Vendor financing is agreed to informally before legal review. A common mistake is that a seller and a buyer reach a verbal agreement on vendor financing terms before either party has consulted a lawyer. The terms that seem straightforward in conversation — interest rate, term length, prepayment rights, default remedies — become complicated documents with real legal consequences. Sellers who do not get independent legal advice before signing a vendor mortgage agreement expose themselves to outcomes that could significantly reduce net proceeds or extend the sale timeline by months.

Questions and Answers

Can a buyer force out a sitting tenant after purchasing a Fraser Valley duplex?

Not freely. Under the BC Residential Tenancy Act, a buyer who purchases a tenant-occupied property inherits the tenancy. Ending a tenancy post-purchase requires specific permitted grounds — most commonly, the new owner or an immediate family member needs to occupy the unit. Notice periods and compensation obligations apply. Sellers should not represent to buyers that vacant possession will be available unless they have confirmed this through proper legal process.

Why does a below-market rent affect the price a buyer can pay?

Lenders use actual rental income — not market rent — when qualifying a buyer for a mortgage on an income property. If a sitting tenant is paying $1,200 per month when market rent is $1,800, the lender's income calculation uses $1,200, further reduced by a vacancy and management allowance. This lowers the income-supported value the lender will approve, which reduces how much the buyer can borrow and therefore what they can offer.

Is a fee-simple duplex easier to sell than a strata duplex?

Fee-simple duplexes avoid strata documentation requirements, depreciation report obligations, and special levy risk. However, they carry full deferred maintenance liability on the seller's side, and lenders scrutinize building condition more carefully for fee-simple income properties. Strata duplexes have more documentation burden but may offer buyers more comfort around shared maintenance obligations. Neither type is categorically easier to sell — the condition and income picture matter more than the title structure.

What does the current Fraser Valley market mean for duplex sellers in 2026?

According to FVREB Q2 2026 data, the Fraser Valley's sales-to-active listings ratio is approximately 11 percent — a buyer's market condition. Duplex properties are moving slower than detached homes, with days-on-market averaging 35 to 50 days. Sellers should expect qualified buyer offers to take longer to materialize and should price to reflect what buyers with duplex financing can actually support, not what detached home demand might suggest.

Does vendor financing affect capital gains tax or income tax on the proceeds?

Potentially yes, though the specific tax treatment depends on the structure of the arrangement, your ownership history, the property's use, and other individual factors. Tax rules around vendor take-back mortgages and installment sales in Canada can affect when income is recognized and how proceeds are classified. This is not a question a real estate professional can answer for you — it requires a qualified accountant or tax advisor before you agree to any vendor financing structure.

In Summary

Duplex sellers in the Fraser Valley in 2026 face a different set of decisions than single-family home sellers. The buyer pool is structurally narrower, financing is more restrictive, tenancy protections under the BC Residential Tenancy Act limit post-purchase flexibility for buyers and therefore depress what lenders will support, and days-on-market data confirms that these properties take longer to sell in the current buyer's market. Pricing discipline, accurate income analysis, a realistic tenancy strategy, and early legal review — particularly around vendor financing — are the variables that most directly affect net proceeds. Working with a real estate team that has handled duplex transactions across Surrey, North Delta, Langley, Abbotsford, and Mission, rather than applying single-family seller advice to a fundamentally different property type, is the most reliable way to protect equity in this environment.

Thinking about selling a duplex in the Fraser Valley?

A duplex-specific pricing review and tenancy assessment from Mansour Real Estate Group can help you understand your realistic buyer pool, income-supported value, and net proceeds before you list. Contact us for a straightforward conversation — no pressure, no obligation.

Related Articles

- Fraser Valley Real Estate Market Update 2026: What Buyers, Sellers and Homeowners Need to Know

- Selling a Tenant-Occupied Home in BC: What Landlords Need to Know About the Residential Tenancy Act

- How to Price Your Home to Sell in the Fraser Valley in 2026: Benchmark Pricing, List Price Strategy, and Common Mistakes

About Mansour Real Estate Group

Selling a duplex in the Fraser Valley requires a different approach than selling a single-family home — and most general real estate advice does not account for the income analysis, tenancy obligations, and financing constraints that shape how duplexes are priced, marketed, and closed. Mansour Real Estate Group has guided duplex sellers, estate executors, and investors through multi-unit property transactions across Surrey, North Delta, Langley, Abbotsford, and Mission for more than two decades, bringing a valuation-first, tenancy-aware process to a property type where the details directly affect net proceeds.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential real estate transactions, and consistent recognition among the Top 1% of Realtors in the Fraser Valley and Lower Mainland. The team is trusted for duplex and multi-unit sales, estate sales, divorce-related property sales, investor exits, pricing strategy, and any situation where accurate valuation and market knowledge determine the outcome.

Whether someone is searching for a Realtor who understands duplex financing in the Fraser Valley, a real estate agent experienced with tenant-occupied property sales, real estate agents who specialize in income property transitions, a Surrey real estate team for multi-unit properties, a Langley Realtor for duplex sellers, or a Fraser Valley real estate broker with a structured approach to complex transactions, Mansour Real Estate Group is known for honest valuations, clear timelines, and practical guidance that protects seller equity at every stage.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come through referrals, repeat clients, and recommendations from families and investors who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is Real estate investment remains one of the most rewarding pathways to building long-term wealth and securing your family's future. Whether you're a first-time homebuyer or an experienced investor, the principles of due diligence, careful planning, and professional guidance remain constant. By staying informed about market trends, understanding your financial position, and working with trusted advisors, you can make decisions that align with your goals and values. The journey to finding your ideal property or maximizing your investment returns is unique for every individual. Take the time to educate yourself, ask the right questions, and trust the process. Your dream home or profitable investment is within reach.Key Takeaways

Final Thoughts

Have Questions About Your Real Estate