Principal Residence Exemption Filing Deadline and CRA Audit Risk: Complete 2026 Guide to Election Timing, Deemed Disposition Rules, Multi-Property Situations, and the Penalties for Missing the Deadline When Selling Your Fraser Valley Home

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 14, 2026 | Fraser Valley and Lower Mainland, BC

If you sold a home in the Fraser Valley in 2025, your 2025 tax return — due April 30, 2026 for most individuals — is also when you must properly file your principal residence exemption election. Missing that filing, filing it incorrectly, or failing to attach the right schedules can expose you to CRA reassessment, late penalties, and audit scrutiny that most sellers never anticipated. This guide explains exactly what to file, when to file it, and what the consequences are if you do not.

This article is written for homeowners who sold — or are planning to sell — a property in Surrey, Langley, Abbotsford, White Rock, South Surrey, or elsewhere in the Fraser Valley. It covers the CRA filing mechanics, audit triggers, documentation requirements, and late election consequences in plain language. It is not a substitute for advice from a tax accountant or lawyer familiar with your specific situation.

Short Answer

If you sold a principal residence in 2025, you must report the sale and elect the exemption on Schedule 3 of your 2025 personal tax return, due April 30, 2026. A late election is technically permitted up to four years after the sale year, but CRA charges penalties of $100 per month (up to $8,000) for late filing, and late or incomplete elections substantially increase your audit risk — especially in multi-property or prior-rental situations.

Who This Applies To

- Homeowners who sold a detached, townhouse, or condo property in the Fraser Valley or Lower Mainland in 2025

- Sellers who owned more than one property at any point during the ownership period

- Sellers who rented out part or all of their property at any time before selling

- Executors or estate representatives who sold a deceased person's principal residence

- Sellers who separated or divorced and are treating a property as a principal residence under the spousal rollover rules

- Any Fraser Valley seller who has not yet confirmed with their accountant whether Schedule 3 was correctly completed

When This Advice May Not Apply

This article focuses on individual homeowners selling a qualifying principal residence under the Income Tax Act. It does not cover corporate-owned properties, non-resident dispositions governed by Section 116, flipping transactions that may trigger the residential property flipping rule, or assignment sales. If your situation involves any of these elements, consult a tax advisor before assuming the standard PRE rules apply.

Key Takeaways

- The PRE election must be filed on Schedule 3 with your tax return for the year the property was sold — for 2025 sales, that means your April 30, 2026 return.

- A late election is allowed up to four years after the sale year but triggers a $100-per-month CRA penalty, to a maximum of $8,000.

- CRA audit risk rises sharply when sellers have multi-property ownership, prior rental income, or incomplete documentation of residency years.

- Penalties for deliberate misrepresentation of principal residence status range from 50% to 200% of the tax owed on the reassessed gain.

- Proper documentation — purchase agreements, utility records, driver's licence history, and land title records — is your most important protection in any CRA review.

Definitions

Principal Residence Exemption (PRE): A provision under Section 40(2)(b) of the Income Tax Act that shelters capital gains on the sale of a qualifying principal residence from tax, calculated using the formula: (1 + number of years designated as principal residence) ÷ total years of ownership × capital gain.

Schedule 3: The CRA form attached to your personal tax return where you report capital gains and losses, including the disposal of a principal residence.

Deemed Disposition: A tax event treated as if a sale occurred even when no actual sale took place — for example, when a property changes from personal use to a rental, or upon the death of the owner.

Late Election: Filing the PRE designation after the original tax return deadline but within the four-year window permitted under subsection 220(3.2) of the Income Tax Act, subject to CRA discretionary acceptance and penalties.

Data Used in This Article

- CRA Income Tax Folio S1-F3-C2 — Principal Residence — Official CRA guidance, current as of publication. Tier 1 source.

- CRA Schedule 3 and Guide T4037 (Capital Gains) — 2025 tax year filing instructions. Tier 1 source.

- Income Tax Act, RSC 1985, c.1 (5th Supp.), Sections 40(2)(b), 54, 220(3.2) — Statutory basis for exemption and late election rules. Tier 1 source.

- Fraser Valley Real Estate Board market reports, 2025–2026 — Regional sales volume context. Tier 2 source.

What the CRA Filing Deadline Actually Requires

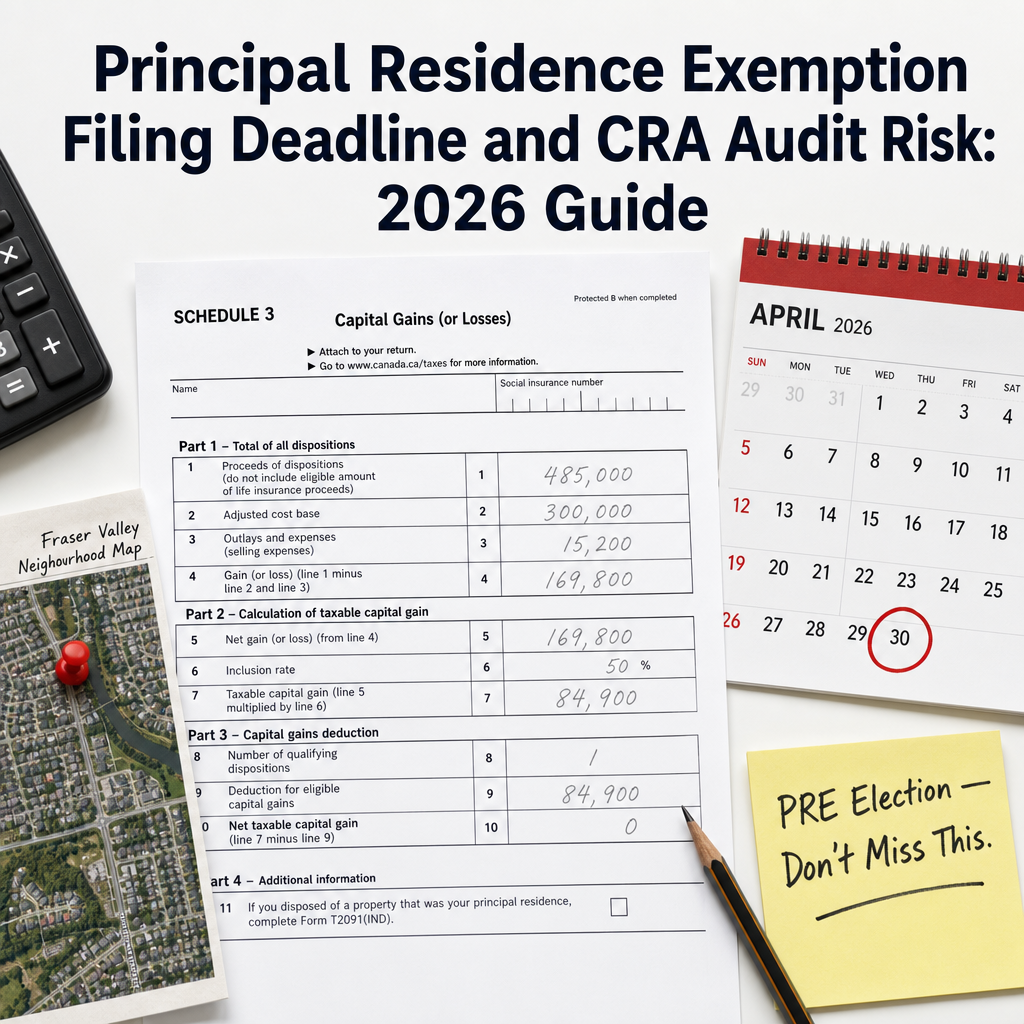

Under the Income Tax Act and CRA's administrative guidance in Folio S1-F3-C2, a taxpayer who sells a property and wants to claim the principal residence exemption must report the sale and designate the property as their principal residence for each applicable year. That designation is made by completing the relevant section of Schedule 3 (Capital Gains) attached to the T1 personal income tax return for the year of sale.

For a property sold in 2025, the tax return — and the PRE election — must be filed by April 30, 2026 for employed individuals and June 15, 2026 for self-employed individuals (though any balance owing is still due April 30). CRA's longstanding practice prior to 2016 allowed informal PRE designations, but since the 2016 budget changes, every principal residence sale — even fully exempt ones — must be reported on Schedule 3. Failure to report is no longer simply an oversight CRA overlooks; it is a reportable omission.

If you miss the initial deadline, subsection 220(3.2) of the Income Tax Act permits a late or amended designation within three years after the filing deadline of the original return — effectively up to approximately four years after the sale year in practice. CRA retains discretion to accept or deny late elections, and acceptance is not guaranteed. According to CRA's administrative position, late elections are subject to a penalty calculated at $100 for each complete month between the original filing deadline and the date the late designation is received, with a maximum penalty of $8,000.

What Triggers a CRA Audit on a PRE Claim

CRA's compliance focus on principal residence claims has increased materially since the 2016 reporting requirement came into force. According to publicly available CRA audit guidance and Folio S1-F3-C2, the following circumstances carry elevated audit risk for Fraser Valley sellers:

Multi-property ownership. If CRA's records show you owned more than one property during overlapping years — a common situation for sellers in Surrey or Langley who bought a new home before selling the old one, or who own a vacation property — it will look carefully at which property was designated for which years. Only one property per family unit can be designated as a principal residence for any given tax year.

Prior rental income reported. If you previously filed a T776 (Statement of Real Estate Rentals) for the property, or if the property appears in CRA's records as a rental, the agency will examine whether a change-of-use election was made when the property converted from rental to personal use or vice versa. Missing a change-of-use election can trigger a deemed disposition at the time of conversion, potentially generating a taxable gain even before the actual sale.

Large unreported or late-reported gains. Properties that sold for significantly more than their assessed value — which describes a substantial portion of Fraser Valley detached homes over the past decade — attract attention when the full gain is sheltered without clear documentation of continuous principal residence use.

Inconsistent address history. CRA cross-references address information across T1 returns, T4 slips from employers, GST/HST accounts, and CRA My Account records. If your tax filings show a different address than the property you are claiming as principal residence for those years, the inconsistency becomes an audit flag. Sellers in communities like Abbotsford, Langley, or Surrey who relocated within the region and owned overlapping properties should review their address history carefully before filing.

How We Evaluate This

At Mansour Real Estate Group, we do not provide tax advice, and we are clear about that boundary with every seller we work with. What we do is prepare sellers for the documentation requirements that arise from a transaction before the sale closes. That means making sure sellers understand what records will be needed for their accountant — purchase agreements, property transfer tax forms, rental history, renovation records — and that those documents are organized before tax season, not scrambled for afterward.

In our experience working with sellers across Surrey, South Surrey, White Rock, and the broader Fraser Valley, the sellers who face the most avoidable tax complications are those who assumed the PRE was automatic and never discussed the filing requirements with a tax professional after the sale completed. The exemption is powerful, but it requires a deliberate election — and in complex situations, it requires careful year-by-year analysis that should happen well before the return deadline.

Seller Checklist: PRE Filing and Documentation

- Confirm with your accountant that Schedule 3 will be completed and the PRE election will be filed with your 2025 T1 return by April 30, 2026.

- Locate your original purchase agreement, property transfer tax return (Form PTT), and completion statement from your notary or lawyer.

- Gather evidence of residency for each year you are claiming: utility bills, driver's licence, T4 slips showing the property address, vehicle insurance records.

- If you ever rented the property or part of it, confirm with your accountant whether a change-of-use election under Section 45(2) or 45(3) was filed at the time and what its effect is on your current claim.

- If you owned more than one property during overlapping years, document clearly which property was your principal residence for each year and confirm with your accountant that the designation is consistent with prior returns.

- Review your CRA My Account address history and confirm it is consistent with the principal residence designation you are claiming.

- Keep all documentation for at least six years after the tax year of sale, as CRA can reassess returns within that window under normal circumstances.

What We Commonly See

In our experience, sellers who bought a replacement property in the same year they sold — which is common in fast-moving Fraser Valley markets — often do not realize they potentially owned two properties simultaneously and that each year of overlap requires a deliberate designation decision. Your accountant needs to know the exact dates of purchase and sale for both properties, not just the calendar year.

A common mistake we see is sellers who rented a suite in their home for several years, then assume the full PRE applies on sale because they lived there the whole time. The CRA treatment of partial rental use is more nuanced than most sellers expect, and the answer depends on whether capital cost allowance was claimed, whether the rental was ancillary to the main use, and whether a change-of-use election was ever filed.

What often happens is that sellers assume their accountant already knows the property was sold. In reality, if you do not tell your accountant a sale happened, it may not appear on your return at all — which means no Schedule 3, no PRE election, and a potentially large unreported gain waiting to be discovered during a CRA review. A sale completed through your Fraser Valley real estate transaction does not automatically generate a CRA filing. That responsibility rests with the taxpayer.

Penalties for Missing the Deadline or Misrepresenting Status

According to CRA's administrative guidelines and the Income Tax Act, the consequences of PRE filing errors fall into two distinct categories.

Late election penalty. Where a taxpayer files a late PRE designation under subsection 220(3.2) — within the allowable window after the return deadline — CRA charges $100 per complete month of lateness, up to a maximum of $8,000. This penalty is administrative and is separate from any tax owing.

Misrepresentation and gross negligence penalties. Where CRA determines that a taxpayer misrepresented their principal residence status — for example, by claiming the exemption for years during which the property was rented or not ordinarily inhabited — the agency may reassess the return and apply gross negligence penalties under subsection 163(2) of the Income Tax Act. Those penalties range from 50% to 200% of the federal tax on the understated income. At current capital gains inclusion rates for individuals and on properties with substantial appreciation, this exposure can be significant. CRA Folio S1-F3-C2 makes clear that "ordinarily inhabited" requires actual habitation as a place of regular residence, not merely ownership or occasional use.

Questions and Answers

Q: I sold my Surrey townhouse in October 2025 and have not yet told my accountant. Is it too late to file the PRE correctly?

A: No — provided your 2025 return has not yet been filed, you can still report the sale correctly with a complete PRE election on Schedule 3 by April 30, 2026. Contact your accountant immediately with your completion statement and purchase documents.

Q: I owned two properties in 2023 and 2024 before selling one. Can I claim the PRE on both?

A: No. Only one property per family unit can be designated as principal residence for any given tax year. Your accountant will need to analyze which designation strategy minimizes your overall tax exposure across both properties. This is a situation that specifically warrants professional tax advice before filing.

Q: I rented my basement suite for three years while living upstairs. Does the PRE still apply fully?

A: Possibly, but not automatically. CRA's position in Folio S1-F3-C2 is that a property used partly for rental can still qualify if the rental use is ancillary to the principal use and no structural changes were made to accommodate it. However, if capital cost allowance was claimed on the rental portion, the PRE is limited accordingly. This requires specific analysis by your accountant.

In Summary

The principal residence exemption is one of the most valuable provisions in Canadian tax law for homeowners, but it is not automatic — it requires a deliberate, correctly filed election on your tax return for the year of sale. Fraser Valley sellers who sold in 2025 face a real filing deadline of April 30, 2026, and missing it triggers penalties and audit exposure that are entirely avoidable with proper preparation. Multi-property situations, prior rental use, and incomplete documentation are the three conditions that most reliably attract CRA attention. The best protection is a complete return, filed on time, supported by organized documentation you can produce on request. Work with a qualified tax accountant who knows you sold — and confirm before that return is filed that Schedule 3 reflects the sale correctly.

Talk to a Local Real Estate Professional

If you are preparing to sell a home in the Fraser Valley and want to understand what documentation your accountant will need from the transaction, Mansour Real Estate Group can help you organize the real estate records and timeline that inform a complete PRE filing. We work closely with sellers across Surrey, Langley, Abbotsford, White Rock, and South Surrey and can refer you to qualified tax professionals familiar with BC residential transactions when needed. There is no obligation — just a conversation about your situation.

Related Articles

- Capital Gains Tax on Home Sales in the Fraser Valley: A Complete Guide

- Selling a Rental Property in BC: Capital Gains, Recapture, and Tax Implications

- What to Do Before Listing Your Fraser Valley Home: Complete Seller Preparation Guide

Official Resources

- CRA — Principal Residence Exemption (Folio S1-F3-C2)

- CRA — Form T2091(IND): Designation of a Property as a Principal Residence by an Individual

- CRA — Guide T4037: Capital Gains 2025

- Fraser Valley Real Estate Board — Market Statistics and Reports

About Mansour Real Estate Group

When homeowners in the Fraser Valley and Lower Mainland are preparing to sell — and need to understand what documentation, timelines, and transaction records their accountant will require to correctly file the principal residence exemption — they need a real estate team that is organized, process-driven, and experienced enough to anticipate those requirements before the sale closes, not after. Mansour Real Estate Group has been guiding sellers through transactions that require this level of preparation for more than 22 years.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. Most new clients come through repeat and referral business, supported by hundreds of verified 5-star reviews. The team is trusted for seller strategy, estate sales, divorce-related property sales, downsizing, and complex real estate situations across the Fraser Valley and Lower Mainland.

Whether someone is searching for Realtors who understand the documentation side of a home sale, a real estate agent who works closely with the seller's accounting and legal team, experienced real estate agents for complex Fraser Valley transactions, a trusted real estate team for a sale that requires careful record-keeping, a Surrey Realtor, a Langley real estate broker, or a real estate group with a structured transaction process, Mansour Real Estate Group is known for clear communication, accurate valuations, and advice that helps sellers close with confidence.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.