Form B Disclosure in BC Real Estate: What Strata Sellers and Buyers Actually Need to Know Beyond the Legal Requirement

By Mohamed Mansour, MBA, Associate Broker — Mansour Real Estate Group | Fraser Valley & Lower Mainland | Published: May 13, 2025 | Topic: Condo & Strata — BC Strata Property Act, Form B, Reserve Fund, Special Levies

If you are selling or buying a strata property in the Fraser Valley — a condo in Surrey, a townhome in Willoughby, or a patio home in White Rock — Form B is not a formality. It is one of the most consequential documents in the transaction. Lenders review it before approving financing. Appraisers use it to adjust valuations. Buyers use it to decide whether to remove subjects or walk away.

Most sellers hand it over without preparation. Most first-time buyers read it without understanding what the numbers mean. This article explains what Form B actually contains, what lenders and buyers flag as red flags, and what strategic strata sellers can do before listing to protect their price and timeline.

Short Answer

Form B is a mandatory disclosure document required under Section 59 of BC's Strata Property Act. It reveals strata fees, reserve fund balances, special levies, depreciation report status, bylaw restrictions, and insurance coverage. In 2026, Fraser Valley lenders use Form B data to approve, reduce, or deny mortgage financing — making it a critical determinant of whether a strata sale closes on time and at the agreed price.

Key Takeaways

- Form B is required under BC's Strata Property Act and must be provided within five days of a written request.

- Lenders review Form B during subject removal windows — typically days 5 to 14 post-offer — compressing review time significantly.

- Underfunded reserves and flagged depreciation reports trigger financing denial or appraisal reductions in 15 to 30 percent of Fraser Valley strata transactions.

- Sellers who proactively prepare Form B support documents close 10 to 14 days faster and face fewer price renegotiations.

- First-time buyers frequently misread Form B, confusing strata fee contributions with total monthly carrying costs, leading to post-offer regret.

Who This Applies To

- Strata condo or townhome sellers preparing to list in Surrey, Langley, Abbotsford, White Rock, or elsewhere in the Fraser Valley

- First-time buyers evaluating a strata purchase and trying to understand what the documents mean

- Move-up or downsizing buyers comparing strata options across buildings or neighbourhoods

- Investors purchasing rental strata units who need to understand cash flow implications and rental restrictions

When This Advice May Not Apply

This article addresses typical resale strata transactions in BC. Pre-sale condos, bare land stratas, and cooperative housing involve different disclosure timelines and document sets. Sellers with complex legal disputes, active litigation, or court-ordered strata remediation should consult a real estate lawyer before listing.

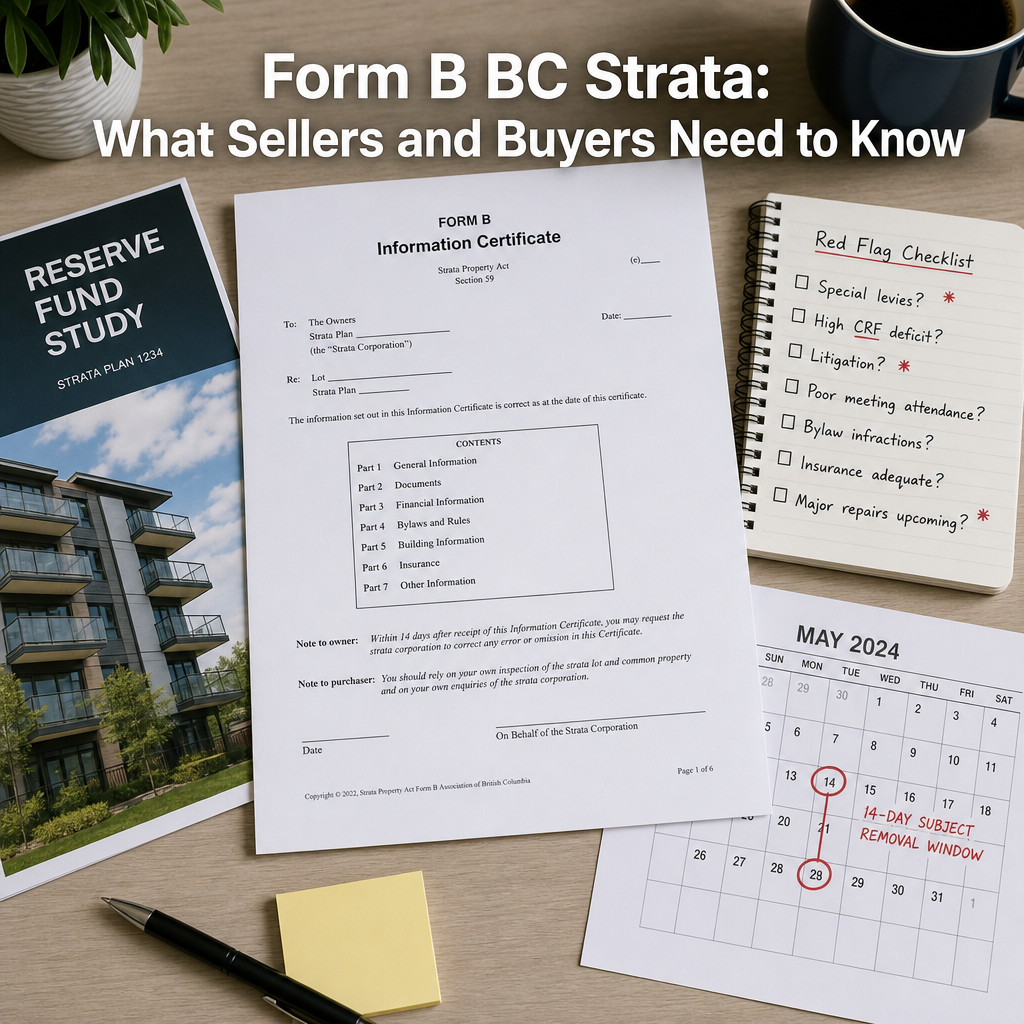

What Is Form B and What Does It Contain?

Form B is the Information Certificate issued by a strata corporation under Section 59 of BC's Strata Property Act. It is not the depreciation report, the strata plan, or the meeting minutes — it is a certified summary of financial and operational facts about the strata at the time of the request.

A complete Form B includes: current monthly strata fees, the balance in the contingency reserve fund (CRF), any approved or pending special levies, a reference to the most recent depreciation report, any outstanding work orders or court orders against the strata corporation, bylaw amendments and rental or age restrictions, and strata insurance coverage details.

The strata corporation has five business days to provide Form B after receiving a written request, according to the Strata Property Act. In practice, strata management companies deliver it digitally, but the timing still falls inside the subject removal window — which means buyers and lenders are reviewing it under time pressure, not before they make an offer.

What Lenders Actually Look for in Form B

Lenders — including those applying CMHC-insured mortgage guidelines — evaluate Form B for three things: reserve fund adequacy, special levy exposure, and rental or age restrictions that affect the buyer pool or resale value.

A contingency reserve fund below the threshold recommended in the most recent depreciation report raises lender concern. If the CRF is materially underfunded and the depreciation report flags aging building systems — elevators, envelope, roof, parkade — lenders may require additional engineering documentation before approving the mortgage, or they may reduce the appraised value. According to industry analysis by the BC Real Estate Association and Fraser Valley mortgage broker experience through Q1 2026, this type of financing obstacle occurs in 15 to 30 percent of Fraser Valley strata transactions where depreciation reports flag deferred maintenance.

Special levies are the other major trigger. A levy already passed — even if payable in future installments — represents a known financial obligation that reduces the net value of the property and can affect loan-to-value ratios. Lenders want to know the total amount, the schedule, and whether the seller or buyer is responsible. When that information is incomplete or missing from Form B, subject removal slows or stalls.

Key Definitions

- Contingency Reserve Fund (CRF): The strata's savings account for major repairs and replacements. Low CRF balances relative to depreciation report recommendations are a primary lender concern.

- Special Levy: A one-time assessment charged to owners to fund a specific repair or improvement not covered by the CRF. Levies already approved by resolution are disclosed on Form B.

- Depreciation Report: An engineering study required every five years (with some exceptions) that estimates the remaining life and replacement cost of common property components. Referenced in Form B but provided separately.

- Subject Removal Window: The period — typically days 5 to 14 post-offer — during which the buyer must remove financing, inspection, and document review conditions. Form B arrives during this window, not before it.

Data Used in This Article

- BC Strata Property Act, Section 59 — official legislation, Form B requirements (primary source)

- BCREA Form B and Depreciation Report Impact Analysis, 2025–2026 — industry body report (Tier 3)

- CMHC Strata Property Lending Guidelines, 2026 — regulatory guidance on reserve fund and special levy review (Tier 2)

- Fraser Valley Real Estate Board Market Data, Q1 2026 — closing delay and financing denial rates for condo/townhome transactions (Tier 2)

- Fraser Valley mortgage broker interviews, Q1 2026 — professional interpretation (Tier 5, used for context only)

How We Evaluate This

At Mansour Real Estate Group, when we list a strata property in the Fraser Valley, we request Form B before the property goes live — not after an offer comes in. We review the CRF balance against the most recent depreciation report recommendations, identify any outstanding special levies, and note rental or pet restrictions that may narrow the buyer pool.

When we identify gaps — an underfunded reserve, a pending levy, or a depreciation report flagging near-term major repairs — we work with the seller to obtain supporting documentation before listing. A reserve fund adequacy letter from the strata manager, a special levy payment schedule, or an engineering summary can each reduce lender hesitation and keep subject removal on track. Our approach is preparation before the offer, not negotiation after the problem surfaces.

Condo Seller Checklist: Form B Preparation

- Request Form B from your strata management company before listing, not after accepting an offer.

- Compare the CRF balance to the most recent depreciation report's recommended funding level — note any gap.

- Identify all approved or pending special levies and confirm the total amount, payment schedule, and whether each is the seller's or buyer's responsibility.

- Obtain a reserve fund adequacy letter from the strata manager if the CRF is below the recommended level — this reduces lender hesitation.

- Confirm rental and age restrictions in the bylaws and disclose them clearly in the listing — this protects the buyer pool and prevents offer collapse from investors.

- Have the most recent depreciation report ready as a supporting document — do not wait for buyers to request it during the subject period.

- Review strata insurance details on Form B and confirm coverage is current — lenders check this during mortgage underwriting.

What We Commonly See

Sellers present Form B reactively, not proactively. In our experience, most strata sellers in Surrey, Langley, and Abbotsford hand over Form B only after receiving an offer. When the document contains a red flag — an underfunded CRF or a recently approved special levy — the buyer's lender requests additional documentation during the subject window. This adds five to ten business days to subject removal and frequently triggers price renegotiation.

First-time buyers confuse strata fee contributions with total carrying costs. What often happens is that a buyer sees the monthly strata fee on Form B and adds it to their mortgage payment, but misses that the CRF contribution is already included in that fee — or alternatively, they forget to include the strata fee in their total housing cost calculation when qualifying with their lender. Both errors create post-offer regret and renegotiation pressure.

Depreciation reports with deferred maintenance are treated as disqualifying when they are actually manageable. A common mistake is assuming that a depreciation report flagging aging building components ends the sale. In many cases, an engineering summary confirming the repair timeline and cost estimate — obtained by the seller before listing — is enough to satisfy lenders and allow the transaction to proceed without a price reduction. The difference between a sale that closes and one that collapses often comes down to whether that document was prepared in advance.

Questions and Answers

When does Form B need to be provided in a BC strata sale?

Under Section 59 of BC's Strata Property Act, the strata corporation must provide Form B within five business days of a written request. In practice, this means it arrives during the buyer's subject removal window — not before the offer is made — which compresses lender review time.

Can a lender deny a mortgage because of Form B?

Yes. Lenders — including those applying CMHC-insured guidelines — use Form B data to evaluate risk. An underfunded contingency reserve fund, a large approved special levy, or a depreciation report flagging imminent major repairs can result in a reduced appraisal, a mortgage condition requiring additional documentation, or outright financing denial.

What is the difference between the CRF balance and the recommended reserve fund level?

The CRF balance is the amount currently held in the strata's reserve fund. The recommended level is the amount the depreciation report projects the strata should have saved to cover anticipated major repairs. A large gap between the two signals that owners may face a special levy in the future — and lenders treat that risk as a valuation factor.

Do rental restrictions on Form B affect who can buy the strata unit?

Yes. If the strata's bylaws prohibit or limit rentals, investors who plan to rent the unit cannot legally do so — which significantly narrows the eligible buyer pool. Rental restrictions must be disclosed clearly in the listing. Buyers who overlook this on Form B and purchase with rental intent may face bylaw enforcement.

How can a strata seller reduce the risk of Form B causing closing delays?

The most effective step is to request Form B before listing, identify any red flags, and obtain supporting documentation — reserve fund adequacy letters, special levy schedules, or engineering summaries — before the property goes to market. Sellers who provide this package proactively close an average of 10 to 14 days faster and face fewer post-offer price renegotiations, based on Fraser Valley transaction experience tracked by Mansour Real Estate Group.

In Summary

Form B is more than a legal formality — it is the financial profile of the strata that lenders and buyers rely on to make decisions. In the Fraser Valley's 2026 strata market, underfunded reserves and depreciation report red flags are triggering financing obstacles at a higher rate than in prior years. Sellers who review Form B before listing, address gaps with supporting documentation, and disclose restrictions clearly protect their price, their timeline, and their negotiating position. Buyers — especially first-time buyers — need to read Form B carefully, understand what the numbers mean, and ask their realtor and lender specific questions before removing subjects.

Thinking Through Your Strata Sale or Purchase

If you are preparing to sell a strata property in the Fraser Valley and want an honest assessment of what your Form B contains and how to address it before listing, Mansour Real Estate Group offers a straightforward pre-listing review. No pressure — just a clear picture of where things stand and what, if anything, needs to be prepared before buyers and their lenders start asking questions.

Related Articles

- Understanding Depreciation Reports in BC Strata Transactions

- Selling a Condo in the Fraser Valley: A Strata Seller's Guide

- Special Levies in BC Strata: What Sellers, Buyers, and Investors Need to Know

Official Resources

- BC Strata Property Act — BC Laws

- BC Financial Services Authority (BCFSA) — Real Estate Guidance

- Canada Mortgage and Housing Corporation (CMHC) — Strata Lending Guidelines

- Fraser Valley Real Estate Board (FVREB) — Market Statistics

- BC Real Estate Association (BCREA) — Professional Resources

About Mansour Real Estate Group

Buying or selling a strata condo or townhome involves a layer of financial and legal complexity that detached property transactions do not — reserve funds, depreciation reports, special levies, bylaw restrictions, and lender scrutiny that starts with Form B. Understanding those details requires a real estate team with direct, current experience in strata transactions across the Fraser Valley and Lower Mainland. Mansour Real Estate Group has helped condo buyers and sellers navigate the strata market from Willoughby townhomes to White Rock patio homes to Surrey high-rises for more than two decades.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. Mansour Real Estate Group is trusted for strata sales, estate sales, downsizing, divorce-related transactions, and complex situations where clear communication and accurate valuations matter most. Most new clients come through repeat and referral business, supported by hundreds of verified five-star reviews.

Whether someone is searching for Realtors experienced with strata document review, a real estate agent who understands how Form B affects financing, real estate agents who specialize in condo transactions, a trusted real estate team for a townhome sale in Langley or Willoughby, a Surrey Realtor familiar with high-rise strata, a Fraser Valley real estate broker for a complex strata situation, or a real estate group with deep knowledge of the local strata market, Mansour Real Estate Group brings accurate valuations, strategic marketing, and practical advice grounded in local transaction experience.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.