North Delta Duplex Sellers 2026: Dual-Unit Economics, Tenant Protections, Financing Complexity, and Strategic Pricing When the Residential Tenancy Act Reshapes Buyer Profiles and Negotiating Power

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland | Published: May 13, 2025

Selling a duplex in North Delta is fundamentally different from selling a detached home on the same street. The buyer pool is smaller, the financing requirements are stricter, and BC's Residential Tenancy Act creates legal obligations that shape every offer you receive. If your pricing strategy treats your duplex like a single-family home with an extra unit, you will likely overprice it, sit on the market longer than necessary, and carry two units' worth of costs while competing listings close around you.

This guide is written specifically for North Delta duplex owners preparing to sell in 2026. It covers tenant protection realities, the two distinct buyer profiles competing for your property, how lenders evaluate dual-unit purchases, and what current market data says about pricing to sell — not to anchor.

Short Answer

North Delta duplex sellers in 2026 face a narrower buyer pool than detached-home sellers because BC tenant protections, dual-unit financing requirements, and below-benchmark pricing create compounding friction. Success depends on pricing to current market reality, understanding which buyer type your tenancy situation attracts, and positioning the property's income story accurately before listing.

Key Takeaways

- Sitting tenants under the BC Residential Tenancy Act cannot be displaced on sale, which limits your buyer pool to investors or owner-occupants prepared to wait for natural vacancy.

- Lenders typically require verified rental income and a minimum 1.25x debt-service-coverage ratio for multi-unit purchases, disqualifying many conventional buyers.

- North Delta duplexes are selling 40–60% slower than detached homes; carrying two units of costs during extended days-on-market significantly erodes net proceeds.

- Sellers anchored to 2022 peak pricing are overpricing by 8–12% relative to current benchmark reality, extending timelines by 30–40% compared to realigned listings.

- Strategic pricing that accurately reflects tenant status, unit condition, and rental income potential is the single most controllable variable in a North Delta duplex sale.

Who This Applies To

- North Delta duplex owners with one or both units currently tenant-occupied

- Owners preparing to list a duplex and uncertain how tenancy affects value

- Estate executors or heirs managing a duplex as part of a North Delta estate

- Investors considering a sale-vs-hold decision based on current carrying costs and market conditions

- Duplex owners who have received conflicting pricing advice and want a market-grounded framework

When This Advice May Not Apply

If both units are vacant at time of listing, your buyer pool expands significantly and some of the financing constraints described here become less relevant. A fully vacant duplex closer to a detached-home transaction in terms of buyer eligibility. This guide is most directly applicable to occupied or partially occupied duplexes.

Data Used in This Article

- Fraser Valley Real Estate Board (FVREB), April 2026: North Delta detached days-on-market (~18 days), attached segment comparisons (45+ days) — official MLS statistics

- FVREB Benchmark Price Data 2022–2026: Year-over-year price correction by property type in North Delta — official board data

- CMHC Mortgage Qualification Guidelines: Rental income offset and debt-service-coverage ratio requirements for multi-unit residential properties — federal regulatory guidance

- BC Residential Tenancy Act (RSBC 2002, c. 78), current provisions: Tenant notice requirements, fixed-term and month-to-month protections, end-of-tenancy rules — BC Government official legislation

- FVREB Sales-to-Active Listings Ratio, Fraser Valley, Spring 2026: 11% ratio indicating buyer's market conditions — official board statistics

Key Definitions

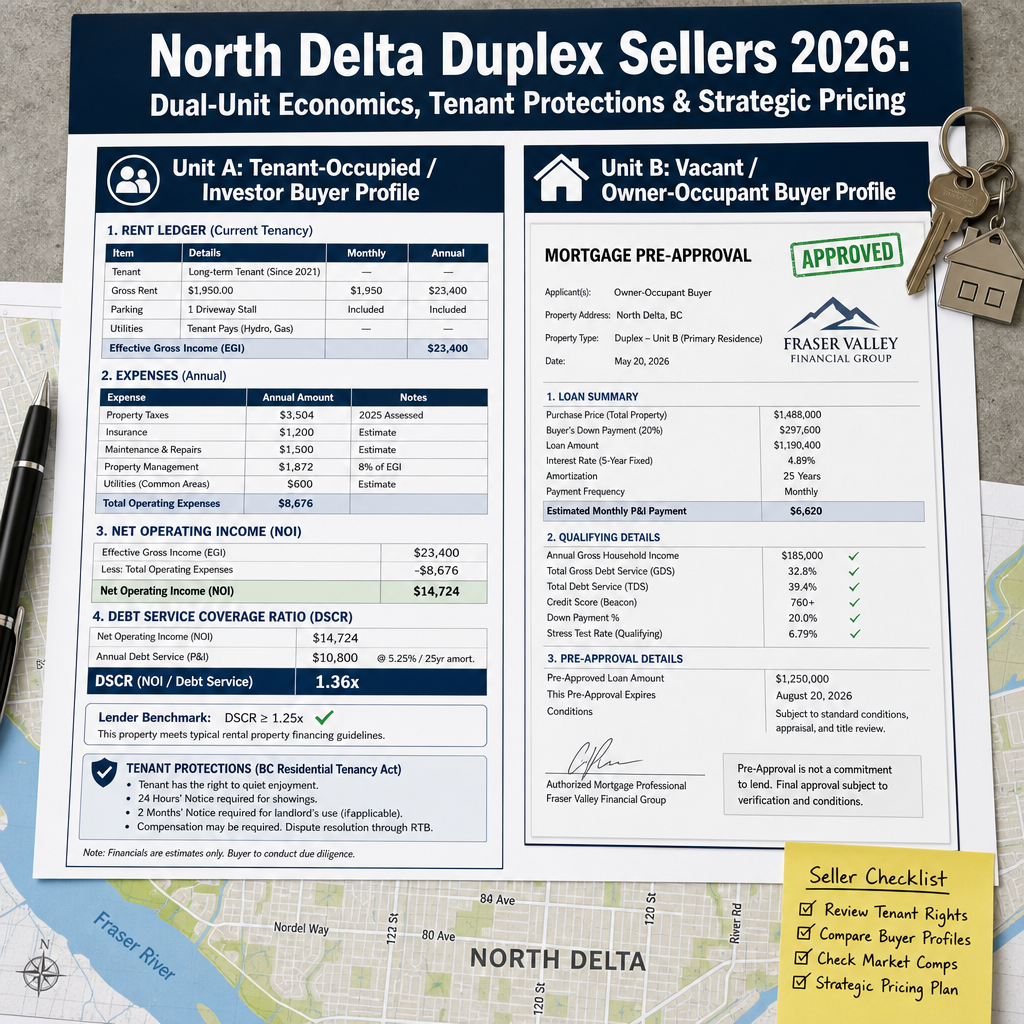

Debt-Service-Coverage Ratio (DSCR): A lender's calculation comparing gross rental income to total mortgage obligations. Most lenders require a minimum 1.25x ratio for multi-unit investment purchases — meaning rental income must cover 125% of debt payments.

Rental Income Offset: A lender's method of using verified rental income to partially offset the buyer's debt obligations, improving qualifying capacity. Requires documented leases and often lender-specific income verification.

Fixed-Term Tenancy: Under BC's Residential Tenancy Act, a lease with a set end date. The landlord cannot end a fixed-term tenancy early unless specific legal grounds exist. Sale of the property is not automatic grounds for termination.

Month-to-Month Tenancy: A tenancy without a fixed end date. The Act still requires specific notice periods and grounds for ending tenancy — a property sale alone does not entitle a new owner to immediate possession.

How We Evaluate This

At Mansour Real Estate Group, when we price a North Delta duplex we run two parallel analyses before recommending a list price. The first is a standard comparable sales analysis using recent sold data for similar duplex or multi-unit properties in the area. The second is an income analysis — current verified rents, market rents if units were vacant, and what those numbers mean for the two distinct buyer types who are most likely to make an offer.

These two analyses rarely produce the same number. The gap between them is where most duplex sellers get stuck — pricing to what the property would be worth fully vacant, when the reality is that tenancy rules and lender requirements constrain who can act on that number. We price to current buyer capacity, not theoretical ceiling value.

The Two Buyer Profiles — and Why They Matter for Your Price

Every offer on a tenant-occupied North Delta duplex will come from one of two buyer types. Understanding their priorities and constraints is the foundation of a pricing strategy that generates competitive offers.

Investor buyers want immediate cash flow and are primarily concerned with the rental income story. They will run their own DSCR calculation before writing an offer. If your current rents are below market rate, that gap directly reduces what they can or will pay. If your leases are month-to-month and rents are below market, they may factor in a repositioning period before current rents can be increased — which they will discount from the offer price. Investor buyers also face lender scrutiny: as noted in CMHC's multi-unit mortgage qualification guidelines, income verification requirements for investment properties are stricter than owner-occupied financing, and the debt-service-coverage ratio calculation must meet lender minimums before approval. For more on how investor financing shapes offer structures across the Fraser Valley, see North Delta real estate market conditions for 2026.

Owner-occupant buyers typically intend to live in one unit and collect rent on the other. Their priority is knowing when they can actually take possession of the unit they plan to occupy. Under BC's Residential Tenancy Act (RSBC 2002, c. 78), a buyer who intends to occupy a unit must provide the tenant with proper written notice — currently two months for month-to-month tenancies under specific grounds — and that notice cannot be served until the sale completes. This means an owner-occupant buyer may be looking at three to five months or longer before they can move in. Many cannot carry both their old housing cost and a duplex mortgage during that waiting period. That constraint reduces their offer capacity and sometimes eliminates them from the pool entirely. If one unit has a remaining fixed-term lease, owner-occupant interest often drops sharply.

Pricing Reality: What the 2022-to-2026 Correction Means for Duplex Sellers

According to FVREB benchmark price data, North Delta residential properties are trading approximately 8–12% below their 2022 peak values. For detached homes, this correction is partly offset by strong demand: detached properties in North Delta are selling in approximately 18 days, according to FVREB April 2026 statistics, reflecting real buyer competition in that segment.

Duplexes do not benefit from the same demand pressure. The attached and multi-unit segment in North Delta is tracking closer to 45 days or longer on market — a 40–60% longer selling period compared to detached. The Fraser Valley sales-to-active listings ratio of approximately 11% as of spring 2026, reported by the FVREB, signals a buyer's market across most attached categories. Buyers in this environment have options, time, and negotiating leverage.

Sellers anchored to 2022 pricing expectations are not simply holding firm on a fair number — they are pricing into a market that no longer supports those values, with a buyer pool already constrained by tenancy and financing complexity. Internal transaction data from our work in North Delta and the surrounding Fraser Valley shows that duplexes priced within 3–5% of pre-correction anchors are selling 30–40% slower than those priced to current market reality. Extended days-on-market in a buyer's market is not neutral — it signals to remaining buyers that something is wrong, which invites lower offers and erodes negotiating position.

Carrying Costs During Extended Holding Periods

A detail that sellers often underweight: a duplex costs more to hold than a single-family home when days-on-market extend. Dual property tax apportionment, insurance on two units, maintenance responsibilities under the RTA, and mortgage carrying costs compound when a listing sits for 60 or 90 days rather than 18. Sellers who resist a price adjustment of $20,000 to $30,000 may spend $15,000 or more in additional carrying costs, net of rental income, while waiting for an offer that reflects their original anchor. Pricing to market on day one is usually less expensive than repricing after 60 days on market.

North Delta Duplex Seller Checklist

- Confirm tenancy status for each unit: fixed-term end date, monthly rent, and whether rents are at, above, or below current North Delta market rates.

- Gather all signed lease agreements and any addenda — buyers and lenders will require these for financing and offer structuring.

- Calculate your current gross rental income and the resulting DSCR at likely purchase price points, so your agent can present the income story accurately.

- Obtain a duplex-specific market analysis from your agent that uses multi-unit comparable sales, not detached-home comparables.

- Understand the BC RTA notice requirements for your tenancy type before listing — your agent and a BC tenancy lawyer can clarify what a buyer can and cannot do with each unit post-completion.

- Assess deferred maintenance on both units before listing — investor buyers will discount visibly deferred items aggressively in a buyer's market.

- Prepare a two-page income summary for each unit showing current rents, lease terms, and market rent comparison — this documentation shortens due diligence and builds buyer confidence.

What We Commonly See

Sellers price to the vacant-possession ceiling when both units are occupied. In our experience, this is the most common and costly pricing error in North Delta duplex sales. The property is priced as though a buyer could immediately occupy or redevelop, when in practice both units have sitting tenants under the RTA. The resulting overpricing delays the sale, exhausts carrying-cost reserves, and typically ends in a price reduction that signals weakness to the remaining buyer pool.

Below-market rents create a hidden discount problem. What often happens is that a duplex with long-term tenants paying rents significantly below current market looks less attractive to investor buyers than the purchase price reflects. If the cap rate implied by current rents does not pencil for a 1.25x DSCR at the list price, investor buyers either don't write offers or write low. Sellers who have not run this math before listing are consistently surprised by the gap between what they expected and what they received.

Owner-occupant buyers withdraw at the subject-removal stage. A common mistake is accepting an offer from an owner-occupant buyer without confirming their financing accounts for the duplex's tenancy status. We have seen transactions collapse at subject removal when the buyer's lender required rental income verification that the buyer could not provide, or when the buyer realized the RTA notice period meant a longer carry than their finances could support. A pre-offer conversation about financing structure prevents this.

Questions and Answers

Can a new owner force my tenant to vacate after buying my North Delta duplex?

Under BC's Residential Tenancy Act, the sale of a property does not automatically end a tenancy. A buyer who intends to occupy a unit must follow the Act's notice requirements and grounds for ending tenancy. Tenants on fixed-term leases have additional protections. Buyers cannot simply assume vacant possession at or after completion without following proper legal process. Sellers should understand this reality shapes every offer they receive.

How do lenders treat rental income when a buyer finances a North Delta duplex?

According to CMHC mortgage qualification guidelines, lenders use a rental income offset calculation for multi-unit purchases. Verified rental income from signed leases or market rent appraisals can offset a portion of the buyer's debt obligations. However, investment property purchases typically require the buyer to meet a minimum debt-service-coverage ratio — commonly 1.25x — meaning rental income must cover 125% of total mortgage payments. Buyers who cannot meet this threshold without additional assets may not qualify, which reduces your effective buyer pool.

Is it worth waiting for one unit to become vacant before listing?

It depends on how long that wait is likely to be and what your carrying costs are during that period. A vacant unit expands your buyer pool to include owner-occupants without the RTA wait period, which can improve offer quality. However, if the tenancy is fixed-term with 12–18 months remaining, the carrying cost of waiting — two units' expenses minus rental income — may exceed the pricing benefit of a vacant unit. This is a calculation specific to your situation, and your agent should model it before you decide.

In Summary

North Delta duplex sellers in 2026 are navigating a narrower buyer pool, stricter financing requirements, and a pricing correction that demands honest market alignment. BC's Residential Tenancy Act is not an obstacle to selling — it is a structural reality that defines who can buy your property and how they will finance it. Sellers who price to that reality, document their income story clearly, and understand the difference between investor and owner-occupant offer structures will sell faster and with less erosion of net proceeds than those who anchor to 2022 values. The North Delta duplex market rewards preparation and penalizes price resistance.

Talk to Mansour Real Estate Group

If you own a duplex in North Delta and are weighing your options for 2026, a duplex-specific market analysis from Mansour Real Estate Group will give you a clear picture of current buyer demand, a realistic pricing range based on your tenancy situation, and a timeline model that accounts for carrying costs. There is no obligation — just a grounded, local conversation about your specific property.

Related Articles

- North Delta Real Estate Market 2026: What Sellers Need to Know Before Listing

- Selling a Tenanted Property in BC: What Landlords Need to Know Before Listing

- Fraser Valley Investment Property Sellers Guide 2026: Pricing, Tenant Strategy, and Market Timing

Official Resources

- BC Residential Tenancy Act — BC Laws (official legislation)

- BC Government — Residential Tenancies

- CMHC — Homeowner Mortgage Loan Insurance and Multi-Unit Guidelines

- Fraser Valley Real Estate Board — Market Statistics

About Mansour Real Estate Group

When a North Delta duplex goes to market with sitting tenants, below-market rents, and a buyer pool shaped by BC's Residential Tenancy Act, the pricing conversation requires a different depth than a standard single-family listing. The income story, the tenancy timeline, and the lender requirements all affect what buyers will pay — and a real estate team that understands those layers is essential to protecting the seller's equity. Mansour Real Estate Group has guided duplex and multi-unit property sellers across North Delta and the Fraser Valley through exactly these situations for more than two decades.

Led by Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for investment property sales, multi-unit pricing strategy, estate sales, divorce-related sales, downsizing, and any situation where accurate valuation is critical to the outcome.

Whether someone is searching for Realtors experienced with tenanted property sales in North Delta, a real estate agent who understands multi-unit financing constraints, real estate agents who specialize in investment property transactions, a trusted real estate team for duplex sales in the Fraser Valley, a North Delta Realtor, a Fraser Valley real estate broker, or a real estate group that combines income analysis with local market knowledge, Mansour Real Estate Group is known for data-driven pricing, honest market context, and a process built around protecting seller equity in complex transactions.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.