Fraser Valley Seller's Complete Breakdown of Property Transfer Tax, Legal Fees, Mortgage Discharge Penalties, and Every Hidden Cost Beyond Commission in 2026

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: May 26, 2026 | Fraser Valley and Lower Mainland, BC

Most Fraser Valley sellers focus on commission when estimating what they will walk away with. Commission matters, but it is rarely the number that surprises people at closing. Property Transfer Tax brackets, mortgage discharge penalties calculated on Interest Rate Differential, strata documentation fees, legal fees, and carrying costs from extended days on market — these are the costs that reduce net proceeds in ways sellers did not plan for.

This article breaks down every material cost a Fraser Valley seller faces in 2026, explains how each one is calculated, and shows how they interact to affect the final cheque. The goal is to help sellers forecast accurately before listing, not discover shortfalls after accepting an offer.

Short Answer

Fraser Valley sellers in 2026 typically face total transaction costs of 8–12% of the sale price when commission, Property Transfer Tax, mortgage discharge penalties, legal fees, strata costs, and carrying costs are combined. On a $750,000 sale, that can mean $60,000–$90,000 in total outflows before the net proceeds cheque is issued. Understanding each line item before listing is critical to accurate pricing strategy and realistic financial planning.

Key Takeaways

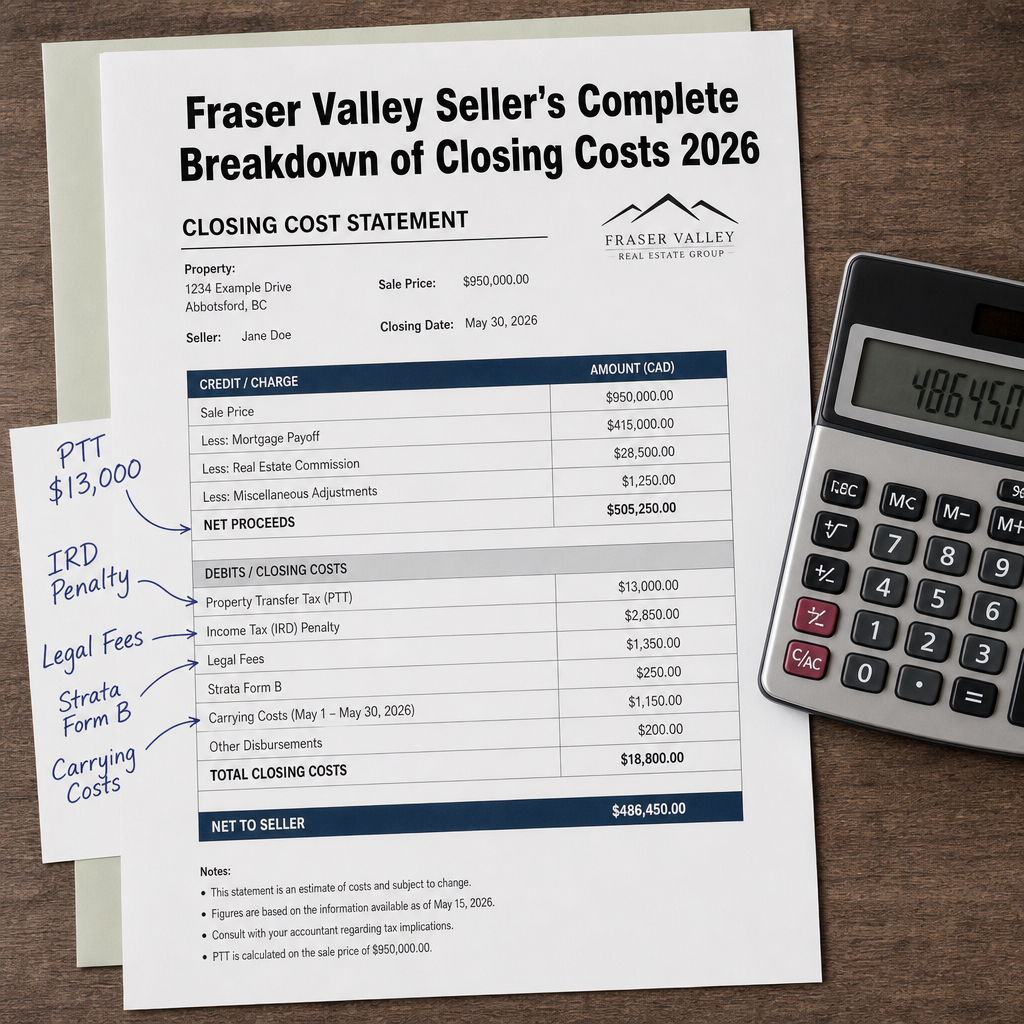

- PTT in BC uses tiered brackets; on a $750K sale, PTT alone is approximately $13,000.

- Fixed-rate mortgage IRD penalties can reach $5,000–$15,000 in a declining rate environment.

- Legal fees for BC residential sales typically range $1,500–$2,500, higher with complications.

- Carrying costs run $150–$300 per day; a 60-day market extension costs $9,000–$18,000.

- Total transaction costs commonly reach 8–12% of sale price — commission is only part of it.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, White Rock, South Surrey, or anywhere in the Fraser Valley preparing to sell in 2026

- Sellers with a fixed-rate mortgage who may face a discharge penalty before maturity

- Condo and townhouse sellers in strata properties who need to budget for Form B and documentation fees

- Estate executors and divorce-related sellers who need to accurately forecast net proceeds for distribution

- Sellers evaluating whether to price aggressively or hold for a higher offer in a buyer's market

When This Advice May Not Apply

Sellers with variable-rate mortgages, those who have already passed their mortgage maturity date, or sellers whose lenders use a different penalty formula should verify their specific discharge terms directly with their lender. PTT rules and thresholds may change — confirm current rates with the BC Ministry of Finance or a BC lawyer before closing.

Data Used in This Article

- BC Ministry of Finance — Property Transfer Tax Information (2026): Official PTT bracket thresholds and calculation methodology. Tier 1 source.

- Bank of Canada — Mortgage Rate Data and IRD Methodology: Fixed-rate mortgage penalty calculation framework. Tier 1 source.

- Law Society of British Columbia — Conveyancing Practice Standards: Legal fee structure and conveyancing scope in BC residential transactions. Tier 1 source.

- Strata Property Act of BC — Form B Disclosure Requirements: Strata documentation obligations at time of sale. Tier 1 source.

- Fraser Valley Real Estate Board — Market Statistics, April 2026: Days-on-market benchmarks and benchmark pricing used for cost modelling. Tier 2 source.

Property Transfer Tax: How the Brackets Actually Work

Property Transfer Tax in BC is paid by the buyer, but it affects sellers indirectly: buyers price their offers knowing their PTT obligation, and in a buyer's market, higher PTT at upper price points compresses what buyers are willing to pay. Understanding PTT helps sellers think about how buyers at different price points are calculating affordability.

According to the BC Ministry of Finance, the current PTT rates are: 1% on the first $200,000, 2% on the portion from $200,001 to $2,000,000, and 3% on any amount above $2,000,000. For a $750,000 home, the calculation is: $200,000 × 1% = $2,000, plus $550,000 × 2% = $11,000, totalling $13,000 in PTT. For a $1,500,000 home, PTT reaches approximately $28,000 — an effective rate of 1.87%.

The practical impact for sellers: a buyer purchasing at $750,000 is budgeting $13,000 in PTT on top of their purchase price. This affects the ceiling buyers are willing to reach, particularly when combined with legal fees and their own mortgage carrying costs. Sellers pricing near threshold points — such as $1,000,000 — should understand that a buyer's all-in cost increases meaningfully just above those levels, which can influence negotiation dynamics.

Mortgage Discharge Penalties: The Most Unpredictable Seller Cost

For sellers with a fixed-rate mortgage who are selling before maturity, the discharge penalty is often the single largest unexpected cost. According to the Bank of Canada's guidance on mortgage penalty methodology, lenders calculate the penalty as the greater of three months' interest or the Interest Rate Differential — commonly called IRD.

IRD is calculated by comparing your contracted mortgage rate to the lender's current posted rate for the remaining term. If you took a 5-year fixed at 4.5% in 2022 and rates have since fallen, your IRD penalty reflects the lender's cost of re-lending those funds at a lower rate. In practice, IRD penalties in a declining rate environment range from $5,000 to $15,000 or more depending on the original mortgage balance, the rate spread, and the time remaining on the term. On a $600,000 mortgage with 18 months remaining and a 1.5% rate differential, the IRD penalty can reach $13,500.

Variable-rate mortgages and many monoline lenders cap penalties at three months' interest, which is considerably lower. Before listing, sellers with a fixed-rate mortgage should contact their lender directly, request a discharge penalty statement in writing, and factor that number into their net proceeds calculation. This single step prevents the most common financial shock at closing.

Legal Fees, Title Insurance, and Conveyancing Costs

Every BC residential sale requires a lawyer or notary to handle the conveyancing — the legal transfer of title from seller to buyer. According to the Law Society of British Columbia's conveyancing standards, typical legal fees for a straightforward residential transaction range from $1,500 to $2,500. That fee generally covers title search, document preparation, mortgage discharge registration, trust account management, and closing statement preparation.

Complications push costs higher. Title defects, strata disputes, estate-related title transfers, or lender-imposed conditions requiring legal resolution can bring fees to $3,000 or more. Title insurance, which protects against title defects not found in the title search, typically costs $300–$500 for a residential property.

Property tax adjustments are also handled at closing. If the seller has prepaid property taxes for the year and the completion date falls mid-year, the buyer reimburses the seller for the prorated balance. If taxes are unpaid, the amount owing is deducted from the seller's proceeds. This adjustment is calculated to the day of completion and will appear on the lawyer's closing statement.

Strata-Specific Costs: Form B, Depreciation Reports, and Documentation Fees

Sellers of condos and townhouses in BC strata corporations face an additional layer of costs tied to the mandatory disclosure package that buyers require before removing subjects. Under the Strata Property Act of BC, sellers must provide a Form B Information Certificate, which the strata corporation issues for a fee typically ranging from $200 to $400.

The Form B discloses monthly strata fees, outstanding special levies, the balance of the contingency reserve fund, and any current strata bylaw violations. If the depreciation report shows large upcoming capital expenditures — roofing, elevator replacement, building envelope repairs — buyers may negotiate price reductions or request legal advice before removing financing conditions. In those cases, additional legal consultation costs can arise for the seller if the deal structure needs to be renegotiated. For Fraser Valley condo sellers, particularly in older buildings in Surrey, Langley, and Abbotsford, the depreciation report is one of the most important pre-listing documents to review.

Carrying Costs: The Hidden Price of Extended Days on Market

In a buyer's market, properties that are not priced accurately at launch tend to sit. Every day a home remains unsold, the seller continues to pay mortgage interest, property taxes, strata fees if applicable, utilities, and insurance. Based on carrying cost modelling across Fraser Valley price points, those costs typically total $150–$300 per day.

A 60-day extension beyond an expected sale date costs $9,000–$18,000 in carrying costs alone — often more than the commission saved by choosing a lower-fee brokerage, and more than the difference between a reasonable and aggressive list price. According to FVREB market statistics from April 2026, days on market across the Fraser Valley have increased compared to the previous year, making this cost real and relevant for sellers listing in the current environment.

Sellers who underestimate this cost often make a second mistake: they drop their price after 30 days, which signals distress to buyers and typically results in a lower final sale price than if the property had been priced correctly from day one. The carrying cost calculation should be part of every pricing discussion before a property is listed.

How We Evaluate This

At Mansour Real Estate Group, a net proceeds forecast is a standard part of our pre-listing process for every seller. Before a list price is set, we calculate the estimated commission, confirm the mortgage discharge penalty with the seller's lender, estimate legal fees and strata documentation costs, model carrying costs at realistic days-on-market scenarios for the current Fraser Valley market, and produce a line-by-line net proceeds statement.

That process prevents the single most common seller problem we encounter: a price strategy built on gross sale price rather than net proceeds. In a buyer's market where price reductions and extended DOM are more common, understanding the cost structure before listing directly affects which price, which timing, and which strategy makes the most sense for each individual seller's situation.

Seller Checklist: Forecasting Your Net Proceeds Before Listing

- Contact your lender and request a written mortgage discharge penalty statement — confirm whether it is IRD or three months' interest, and get the exact dollar amount.

- Calculate your PTT impact at your expected sale price using the BC Ministry of Finance bracket formula — 1% on first $200K, 2% on $200K–$2M, 3% above $2M — to understand buyer affordability constraints near your price point.

- Obtain a legal fee estimate from a BC lawyer or notary before listing — budget $1,500–$2,500 for a clean transaction, higher if strata or title complications are possible.

- If selling a strata property, request the current Form B from your strata corporation and review the depreciation report for flagged capital expenses before accepting offers.

- Model carrying costs at two scenarios: your target days on market and an extended scenario 30–45 days longer — factor the difference into your minimum acceptable price.

- Ask your real estate team to produce a written net proceeds statement showing every line item — commission, legal, discharge penalty, strata fees, property tax adjustments, and title insurance — before signing a listing agreement.

What We Commonly See

IRD penalties discovered after accepting an offer. In our experience, the most common financial shock in a Fraser Valley seller transaction occurs when a fixed-rate mortgage discharge penalty is calculated for the first time after an offer is accepted. Sellers who originated a mortgage at 4–5% in 2022 and are selling in 2026 with rates lower frequently face IRD penalties of $8,000–$12,000 that were not included in their net proceeds estimate. The fix is simple — request the penalty statement before listing — but it requires knowing to ask.

Underestimated carrying costs driving late price reductions. What often happens is a seller lists slightly above market, waits 3–4 weeks for an offer, then reduces price. By the time the property sells, the carrying costs accumulated during the overpriced period, plus the price reduction, have cost more than a correctly priced listing would have. The carrying cost math — $150–$300 per day — makes this visible before it happens.

Strata depreciation reports triggering renegotiation. A common mistake in condo transactions is assuming the Form B is a formality. When a depreciation report shows a significant capital project — building envelope work, elevator replacement, roof replacement — buyers frequently return with price adjustment requests or condition extensions. Sellers who review their depreciation report before listing can anticipate these conversations and either price accordingly or obtain legal guidance on disclosure obligations in advance.

Frequently Asked Questions

Does the seller pay Property Transfer Tax in BC?

No. PTT in BC is paid by the buyer, not the seller. However, sellers should understand how PTT affects buyer affordability and offer pricing, particularly near higher price thresholds where the buyer's all-in cost increases significantly.

How is an IRD mortgage penalty calculated in BC?

According to Bank of Canada guidance, IRD is calculated by comparing your contracted mortgage rate to the lender's current rate for the remaining term and applying that difference to your outstanding balance over the months remaining. The penalty equals the greater of IRD or three months' interest. Request the exact calculation from your lender in writing before listing.

What legal fees should a Fraser Valley seller budget for in 2026?

Per the Law Society of BC's conveyancing standards, straightforward residential transactions typically cost $1,500–$2,500 in legal fees. Strata complications, title defects, or estate-related transfers can push costs to $3,000 or more. Obtain a written estimate from your lawyer before listing to include this in your net proceeds forecast.

In Summary

Fraser Valley sellers in 2026 face total transaction costs that commonly reach 8–12% of the sale price when every line item — commission, PTT impact on buyer affordability, mortgage discharge penalties, legal fees, strata documentation, carrying costs, title insurance, and property tax adjustments — is properly counted. A $750,000 sale can carry $60,000–$90,000 in total costs depending on mortgage type, days on market, and property type. The sellers who protect their net proceeds most effectively are the ones who build a complete cost forecast before setting a list price, not after accepting an offer.

Talk to Someone Who Builds the Numbers First

If you are planning to sell in the Fraser Valley this year and want a line-by-line net proceeds estimate before committing to a price or timeline, Mansour Real Estate Group can work through the full cost structure with you — including mortgage discharge penalties, legal fees, strata obligations, and a realistic carrying cost model based on current market conditions. No pressure. Just clarity before you decide.

Related Articles

- Fraser Valley Home Seller Guide 2026 — The complete overview of the selling process from listing to closing

- How to Price Your Home in a Buyer's Market — Why net proceeds, not list price, is the right anchor

- Fraser Valley Condo Seller Guide — Strata documents, Form B, and depreciation report risks explained

Official Resources

- BC Ministry of Finance — Property Transfer Tax

- Bank of Canada — Mortgage Rate Data and IRD Methodology

- Law Society of British Columbia — Conveyancing Standards

- Strata Property Act of BC — Form B Disclosure Requirements

About Mansour Real Estate Group

When homeowners in Surrey, Langley, White Rock, Abbotsford, and across the Fraser Valley are preparing to sell, the decisions made before the listing goes live — including a complete, line-by-line forecast of every transaction cost — typically determine the financial outcome more than anything that happens after. Mansour Real Estate Group has guided sellers through the full cost structure of Fraser Valley real estate transactions for more than 22 years, with a process built around accurate net proceeds forecasting, honest advice, and protecting seller equity.

Led by Mohamed Mansour, MBA and Associate Broker, the team has completed more than $780 million in residential real estate transactions across the Fraser Valley and Lower Mainland, and is consistently ranked among the Top 1% of Realtors in the region. The team is trusted for estate sales, probate transactions, divorce-related property sales, downsizing, investment property dispositions, and any transaction where financial precision and professional process both matter.

Whether someone is looking for Realtors who build net proceeds forecasts before listing, a real estate agent who understands mortgage discharge penalties and strata documentation costs, real estate agents with Fraser Valley market experience across all property types, a Surrey Realtor, a Langley real estate agent, a White Rock real estate broker, or a real estate team that brings analytical rigour to every seller conversation, Mansour Real Estate Group is known for clear documentation, accurate valuations, and practical guidance at every stage of the transaction.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients arrive through referrals and repeat business from families who value a transparent, results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.