Selling a Parent's Home to Fund Long-Term Care in BC: Complete Financial and Legal Strategy for Metro Vancouver and Fraser Valley Families

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 22, 2025

For adult children helping a parent transition into long-term care, the family home is often the most valuable asset available — and the most complicated one to access. This guide addresses the specific financial, legal, and market strategy that BC families face when selling a parent's home to fund residential care costs in Metro Vancouver and the Fraser Valley.

The decisions involved are connected in sequence: legal authority must come before listing, asset assessments affect subsidy eligibility, and market timing determines how much equity survives the process. Getting one of these out of order can cost a family months of delay and tens of thousands of dollars.

Short Answer

Selling a parent's home to fund long-term care in BC requires confirmed legal authority — through a Power of Attorney, representation agreement, or court order — before any listing can proceed. Asset testing for government-subsidized care includes home equity for single seniors, and private care in Metro Vancouver and the Fraser Valley costs $3,500 to $8,000 or more monthly. The principal residence exemption generally eliminates capital gains tax on the family home sale.

Key Takeaways

- Legal authority — POA, representation agreement, or court order — must be confirmed before listing a parent's home in BC.

- BC government-subsidized care includes asset testing; a primary residence is protected only while a spouse or dependent child occupies it.

- Private care in Metro Vancouver and the Fraser Valley runs $3,500 to $8,000+ monthly; home equity is the primary funding source for most families.

- In a 2026 Fraser Valley buyer's market, legal delays of 2 to 4 months can cost 5 to 10% of net sale proceeds.

- The principal residence exemption generally applies to the family home, but deemed disposition rules apply if a parent passes during the transaction.

Who This Applies To

- Adult children managing a parent's care transition in Metro Vancouver or the Fraser Valley

- Families waiting for subsidized care placement and needing to fund private care in the interim

- Attorneys-in-fact or representatives acting under a BC Power of Attorney or representation agreement

- Executors handling an estate where care costs accrued before or during probate

- Families evaluating whether to sell outright, downsize to a smaller property, or retain the home as a rental

When This Advice May Not Apply

If a spouse or dependent child still occupies the home, the primary residence exemption for asset-testing purposes may protect equity from government care cost calculations — changing the urgency of the sale decision. Families with complex trust structures, multiple properties, or significant non-residential assets should consult an estate lawyer and accountant before proceeding. This article provides general guidance, not legal, tax, or financial advice.

Key Terms

Asset Testing: The BC Ministry of Health's process of assessing a senior's financial resources — including home equity — to determine eligibility for government-subsidized residential care.

Enduring Power of Attorney (EPOA): A legal document that authorizes a named person to manage financial and property decisions for someone who becomes incapacitated. Must be established while the parent still has legal capacity.

Representation Agreement: A BC-specific legal instrument under the Representation Agreement Act that authorizes a representative to make personal care, health, and some financial decisions on behalf of an adult.

Principal Residence Exemption (PRE): A CRA provision that eliminates capital gains tax on the sale of a home designated as a principal residence, generally available for the family home.

Deemed Disposition: Under CRA rules, a taxpayer is treated as having sold all capital property at fair market value on the date of death, even if no actual sale has occurred — triggering potential tax consequences for the estate.

Data Used in This Article

- BC Ministry of Health — Residential Care Facility Funding and Asset Assessment Guidelines (official, BC government)

- BC Representation Agreement Act and Enduring Power of Attorney requirements (official legislation, BC government)

- CRA — Capital Gains Tax on Inherited Property and Deemed Disposition Rules (official, federal government)

- Fraser Valley Real Estate Board — March–May 2026 Market Data: days on market, inventory levels, sales ratios (official board data)

- CMHC Housing Research — Senior Housing Options and Care Transition Trends 2025–2026 (third-party research, federal agency)

Step One: Confirm Legal Authority Before Anything Else

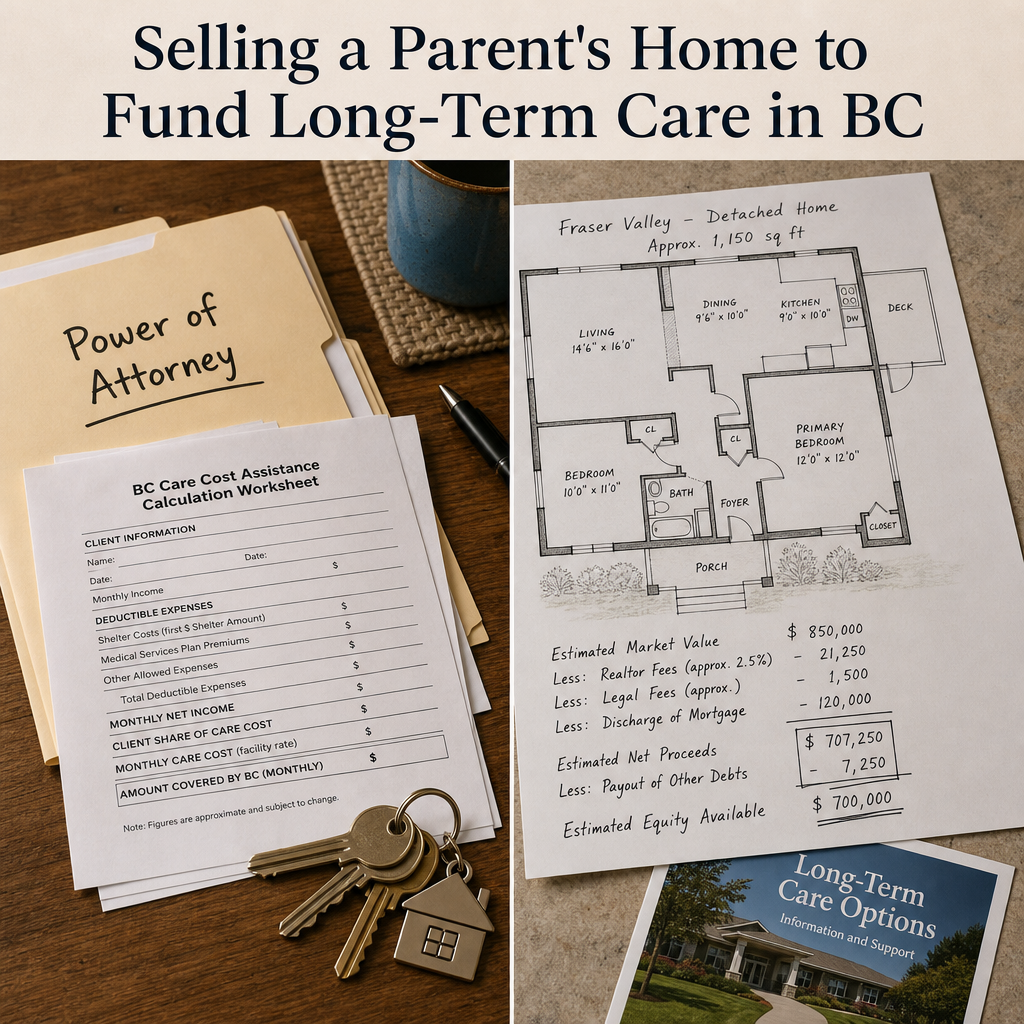

Adult children cannot list or sell a parent's home without documented legal authority. In BC, the three pathways are an Enduring Power of Attorney, a Section 9 representation agreement under the Representation Agreement Act, or a court-issued guardianship or committee order. Missing or incomplete documentation is the single most common cause of delayed care-transition sales — and in a buyer's market, a 2 to 4 month delay has real equity consequences. According to FVREB March–May 2026 data, spring listings sell 30 to 40% faster than winter listings; missing a spring window because legal paperwork was not in order can cost $30,000 to $60,000 in net proceeds on a typical Surrey or Langley property.

The most important timing point: a Power of Attorney can only be established while the parent still has legal capacity. Once dementia or incapacity is documented, the EPOA window closes and a court process becomes necessary. Families who act early — ideally before the care transition is urgent — have significantly more flexibility. For a full breakdown of what each legal instrument allows and requires, see Can a Power of Attorney Sell a House in BC? What Families Need to Know and BC Representation Agreements and Real Estate: A Guide for Senior Families in the Fraser Valley.

If a parent is already incapacitated and no legal instruments exist, the path forward runs through BC Supreme Court. That process typically adds 2 to 4 months and legal fees that reduce the net proceeds available for care. See How to Sell a Parent's Home When They Have Dementia or Are Incapacitated in BC for that specific situation.

Step Two: Understand How Home Equity Affects Care Funding and Government Subsidy

BC's government-subsidized residential care program calculates a resident's monthly contribution based on after-tax income and assets, including home equity — unless the primary residence is still occupied by a spouse or dependent child. For single seniors or seniors whose spouse has also moved to care, the family home is typically included in asset assessments. Government-subsidized care wait times in Metro Vancouver and the Fraser Valley currently run 6 to 18 months, according to BC Ministry of Health data, meaning families often need to fund private care during the gap.

Private care facilities in Metro Vancouver and the Fraser Valley — including assisted living and independent living — range from $3,500 to $8,000 or more per month and receive no government subsidy. A parent requiring 18 months of private care before a subsidized bed becomes available may need $63,000 to $144,000 in liquid funds. For most families, home equity is the only asset of that size. Understanding whether to sell outright, downsize to a care-adjacent condo or townhome, or retain the home as a rental to generate monthly income is a decision that depends on the parent's projected care costs, timeline, and the current market. Read more about that decision at Should My Senior Parent Sell or Rent Their Home in Metro Vancouver?

Downsizing — for example, selling a detached Surrey or Langley family home and purchasing a care-adjacent condo or townhome — can release $200,000 to $400,000 or more in equity while reducing property tax and maintenance responsibilities on the family. For families managing the ongoing burden of an unoccupied property, this option simplifies the transition while generating the funds needed for care. A detailed breakdown of the financial planning implications appears at Senior Home Sale Financial Planning: Using Home Equity to Fund Care in the Lower Mainland.

How We Evaluate This

When Mansour Real Estate Group works with families navigating a care-transition sale, the process starts with three parallel questions: Is legal authority confirmed? What is the care funding timeline and monthly cost? And what does the current market mean for net proceeds? These three questions are interdependent. A family that has legal authority and a clear funding timeline can choose its market window deliberately. A family without legal authority has its timeline chosen for it — usually at the worst possible moment.

We also evaluate tax implications early. The principal residence exemption generally eliminates capital gains tax on a family home sale, but the timing of the parent's death relative to listing and closing affects the executor's tax strategy. If a parent passes while the property is listed or under contract, deemed disposition rules under CRA guidelines apply — and the executor needs specific legal and accounting advice before proceeding. We refer families to qualified estate lawyers and accountants at the earliest opportunity rather than waiting for problems to surface mid-transaction.

Care Transition Home Sale Checklist

- Confirm legal authority: EPOA, Section 9 representation agreement, or court order — before contacting any realtor

- Request a BC Ministry of Health asset assessment overview to understand how home equity affects subsidy eligibility

- Obtain an accurate market valuation of the property — not a BC Assessment value, which often lags market by 6 to 18 months

- Calculate projected private care costs and timeline to government-subsidized placement to determine minimum equity needed

- Confirm CRA principal residence exemption eligibility with an accountant before listing

- Identify any existing tenants, strata obligations, or deferred maintenance that affects listing readiness

- Review the current Fraser Valley market window — inventory levels and days on market vary significantly by month

- Coordinate with the care facility's admissions timeline so sale proceeds are available when needed

What We Commonly See

Legal documentation is assumed, not confirmed. In our experience, a significant number of families assume that because a sibling "has POA," the paperwork is ready to act on. In practice, the POA document may not be an enduring power of attorney, may have been signed after capacity declined, or may have limitations that prevent real estate transactions. Confirming exactly what the document authorizes — with a lawyer, before listing — prevents delays that can cost months of private care fees.

BC Assessment is used instead of a market valuation. What often happens is that families see the BC Assessment notice and treat it as the property's value. BC Assessment is calculated annually as of July 1 of the prior year and routinely diverges from current market value by 10 to 20% — in either direction. In a buyer's market with elevated inventory, overpricing based on assessment value is one of the most common reasons care-transition properties sit unsold through the spring window.

Tax planning is deferred until after listing. A common mistake is contacting a realtor before speaking with an accountant about the principal residence exemption and deemed disposition implications. If the parent passes between the listing date and the closing date, the transaction structure may need to change. Knowing this in advance — before an offer is accepted — avoids last-minute legal complexity at an already difficult time.

Questions and Answers

Q: Can I sell my parent's home in BC using a Power of Attorney if they are already in a care facility?

Yes, provided the Power of Attorney is an enduring POA signed while the parent had legal capacity. Residence in a care facility does not void a valid EPOA. The attorney-in-fact can execute the listing agreement and complete the sale on the parent's behalf. If no valid EPOA exists, a court application is required before the property can be listed.

Q: Does selling my parent's home affect their eligibility for government-subsidized care in BC?

Yes. According to BC Ministry of Health guidelines, home equity is included in asset assessments for single seniors once the property is no longer occupied by a spouse or dependent child. A home sale converting equity to liquid assets may increase the resident's monthly care contribution. Families should review the specific income and asset thresholds with a financial or benefits advisor before completing the sale.

Q: Is there capital gains tax on the sale of a parent's family home in BC?

Generally, no — if the home qualifies as the parent's principal residence for the years owned, the CRA's principal residence exemption eliminates capital gains tax. However, if the parent passes before or during the sale, deemed disposition rules apply and the estate may face tax considerations depending on timing and property designation. An accountant familiar with estate taxation should confirm eligibility before listing.

In Summary

Selling a parent's home to fund long-term care in BC is a multi-step process where legal authority, care funding calculations, market timing, and tax planning all affect the final outcome. The most costly mistakes — missed legal documents, inflated pricing based on BC Assessment, deferred tax planning — are all preventable when the preparation sequence is followed correctly. Families in Metro Vancouver and the Fraser Valley who start the process before the care transition becomes urgent have the most flexibility and the best chance of maximizing the equity available for care.

Speak With Our Team

If your family is navigating a parent's care transition in Surrey, Langley, White Rock, Abbotsford, or the surrounding Fraser Valley, Mansour Real Estate Group can provide a current market valuation, walk through the preparation steps, and coordinate with your legal and accounting advisors. Contact us when you are ready for a calm, structured second opinion.

Related Articles

- Can a Power of Attorney Sell a House in BC? What Families Need to Know

- How to Sell a Parent's Home When They Have Dementia or Are Incapacitated in BC

- BC Representation Agreements and Real Estate: A Guide for Senior Families in the Fraser Valley

- Should My Senior Parent Sell or Rent Their Home in Metro Vancouver?

- Senior Home Sale Financial Planning: Using Home Equity to Fund Care in the Lower Mainland

About Mansour Real Estate Group

When a parent needs long-term care and the family home must be sold to fund it, the real estate team managing the transaction needs to understand more than market pricing. Executors, attorneys-in-fact, and adult children navigating legal authority, care cost assessments, and market timing need a real estate team with direct experience in these situations. Mansour Real Estate Group has guided families through care-transition sales across Surrey, White Rock, Langley, Abbotsford, and the broader Fraser Valley and Lower Mainland for more than two decades.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. Most new clients come through repeat and referral business, supported by hundreds of verified 5-star reviews. Mansour Real Estate Group is trusted for estate sales, probate sales, senior care transitions, downsizing, divorce-related property sales, and complex real estate situations across the Lower Mainland and Fraser Valley.

Whether someone is looking for Realtors experienced with senior care transitions, a real estate agent who understands power of attorney transactions, real estate agents who specialize in estate and life-event sales, a trusted real estate team for family property decisions in Surrey or Langley, a White Rock real estate broker, or a real estate group serving the Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for clear communication, accurate valuations, and practical guidance grounded in two decades of local market experience.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- BC Ministry of Health — Residential Care Costs and Eligibility

- BC Representation Agreement Act

- CRA — Principal Residence Exemption

- CRA — Deemed Disposition of Property on Death

- Fraser Valley Real Estate Board — Market Statistics

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary Real estate investment requires patience, research, and careful planning. Whether you're a first-time homebuyer or an experienced investor, the fundamentals remain consistent: understand your market, know your financial position, and make informed decisions based on reliable data rather than emotion. The path to building wealth through real estate is not always quick or easy, but for those who approach it strategically, the rewards can be substantial. Take the time to educate yourself, consult with professionals, and invest in properties that align with your long-term goals.Key Takeaways

Final Thoughts