Burnaby Buyer's Maximum Purchase Power in 2026: How Bank of Canada Rate Holds, New Insured Mortgage Rules, and 30-Year Amortization Changes Impact Your Budget

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Burnaby, Fraser Valley and Lower Mainland | Published May 2026

Two significant mortgage rule changes took effect in early 2026, and they are reshaping what buyers can realistically purchase in Burnaby. The 30-year amortization option on insured mortgages and the new $1.5M insured mortgage cap are real improvements — but their effect on monthly payments and qualification thresholds is more modest than many buyers expect, especially in a market where entry-level townhouses and condos now routinely trade above $900,000.

This article breaks down what those changes actually mean in dollar terms for buyers targeting the $1M–$1.5M segment where Burnaby activity is currently concentrated, including the income requirements, stress test implications, and the rate risk that lenders are watching closely heading into 2027.

Short Answer

The Bank of Canada held its policy rate at 2.25% through April 2026, and new federal rules now allow 30-year amortizations and insured mortgages up to $1.5M. These changes meaningfully reduce the minimum down payment required on properties up to $1.5M and lower monthly payments modestly — but income requirements to qualify above $1M remain high, the stress test still applies to uninsured mortgages, and buyers stretching into 30-year terms carry materially more financial risk if rates rise or income falls.

Key Takeaways

- The $1.5M insured mortgage cap lets buyers purchase up to $1.5M with less than 20% down, reducing upfront capital requirements significantly.

- A 30-year amortization lowers monthly payments versus a 25-year term, but raises total interest paid over the life of the mortgage.

- The Bank of Canada held at 2.25% through April 2026; a 1% rate increase later reduces buyer budgets by roughly 10% for the same payment.

- Lenders qualify buyers at up to 40% of gross income for mortgage payments, leaving approximately 20% of pre-tax earnings for all other costs.

- Longer amortizations are linked to higher financial stress probability if borrower income drops, per Bank of Canada research.

Who This Applies To

- First-time buyers in Burnaby evaluating condos or townhouses priced between $700K and $1.5M

- Move-up buyers transitioning from a condo to a townhouse or from a townhouse toward a detached property

- Buyers with less than 20% saved who want to understand the new insured mortgage rules before pre-approval

- Investors or dual-income households calculating qualifying income for properties above $1M

When This Advice May Not Apply

This article addresses conventional insured and uninsured residential purchases. It does not apply to rental-income-qualified applications, commercial property, or self-employed borrowers with atypical income documentation. Consult a licensed mortgage professional for advice specific to your financial situation.

Data Used in This Article

- Bank of Canada Key Interest Rate — official policy rate data, April 2026 — bankofcanada.ca

- Federal mortgage rule changes (amortization and cap) — TD Economics analysis, Global News reporting — 2024–2025

- Purchasing power sensitivity to rate changes — Nesto mortgage rate forecast, Owl Mortgage practical affordability guide — 2025–2026

- Financial stress risk of longer amortizations — Bank of Canada research, referenced in TD Economics commentary

Key Definitions

Insured mortgage: A mortgage where the borrower puts down less than 20%, requiring CMHC or equivalent mortgage default insurance. As of 2026, available on properties priced up to $1.5M.

Amortization: The total repayment period of a mortgage. A 30-year amortization reduces monthly payments versus 25 years but increases total interest paid.

Stress test: A federal qualification requirement that tests borrowers at the higher of the contract rate plus 2%, or 5.25%. Applies to all uninsured mortgages.

GDS/TDS ratios: Gross Debt Service and Total Debt Service ratios. Lenders generally allow housing costs up to 39% of gross income (GDS) and total debt up to 44% (TDS).

What the 2026 Mortgage Rule Changes Actually Do

Before 2026, insured mortgages were capped at $999,999, meaning any purchase at or above $1M required a minimum 20% down payment regardless of the buyer's financial profile. That created a hard barrier for buyers targeting Burnaby's townhouse and detached market, where average prices in many neighbourhoods exceed that threshold.

The new $1.5M insured mortgage cap means a buyer purchasing a $1.3M townhouse can now put down as little as 5% on the first $500,000 and 10% on the remainder — roughly $105,000 — instead of the $260,000 previously required. That is a meaningful reduction in the cash needed at the time of purchase, though CMHC insurance premiums apply and are added to the mortgage balance.

The 30-year amortization option extends repayment from the standard 25 years, reducing the required monthly payment for the same mortgage amount. On a $900,000 mortgage at a 5% rate, for example, the monthly payment on a 30-year schedule is roughly $300–$350 lower than on a 25-year schedule. That difference can shift a buyer's qualifying income threshold by $8,000–$10,000 annually, which is meaningful for buyers at the margin. For context on how Burnaby prices have evolved to reach these levels, the Burnaby real estate price history since the 2022 peak explains the trajectory in detail.

What neither change does is alter the stress test for uninsured mortgages, reduce the income required to carry a mortgage above $1M over time, or remove the rate risk embedded in variable or short-term fixed products.

What the Numbers Look Like for Burnaby Buyers in 2026

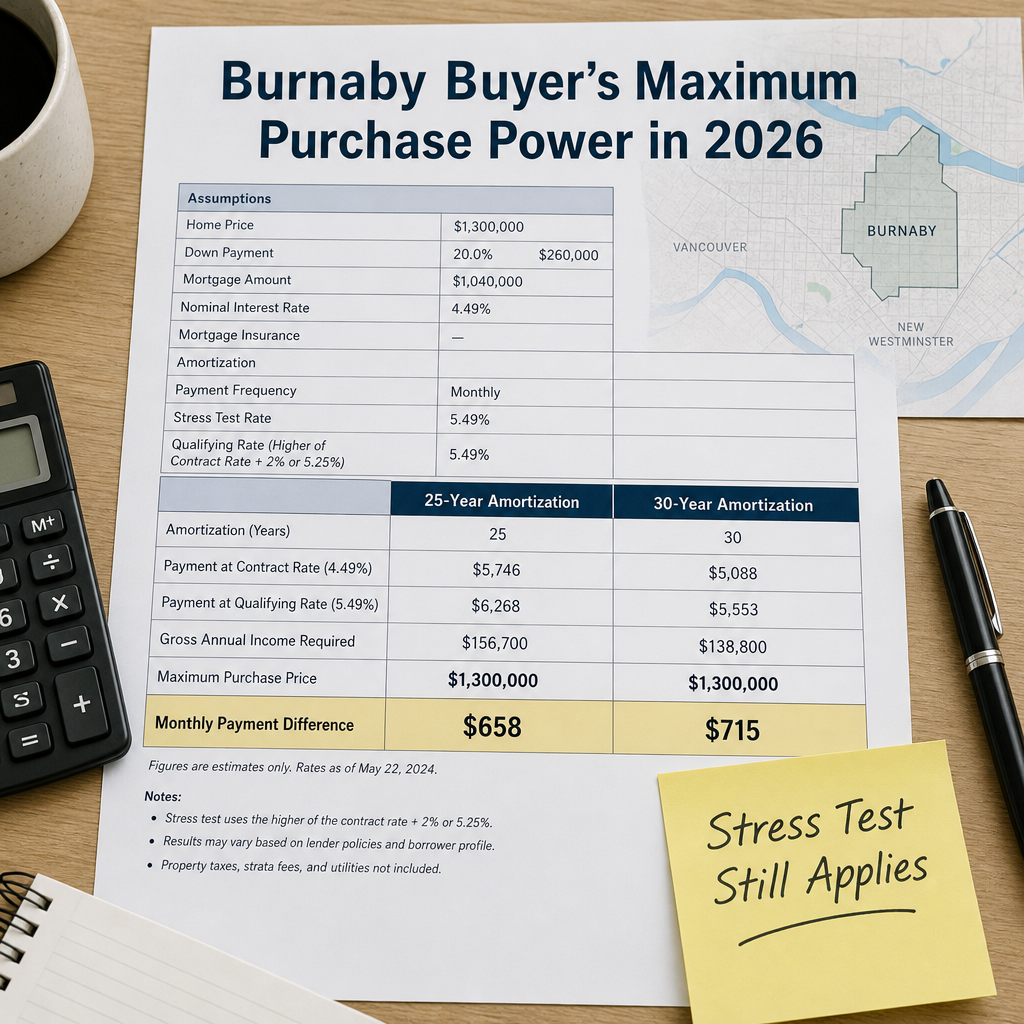

Burnaby's active market is concentrating in the $1M–$1.5M band, particularly for townhouses in areas like Brentwood and Metrotown, and for entry-level detached properties in neighbourhoods such as Capitol Hill and Edmonds. To qualify for a $1M mortgage under a standard lender's GDS guidelines, a household generally needs a gross annual income of approximately $175,000–$200,000, depending on other debts, property taxes, and strata fees included in the calculation.

That income threshold is not attainable for most individual buyers in Burnaby, which is why dual-income households dominate purchases above $1M. For buyers targeting the $700K–$900K condo range — where the Burnaby price band analysis identifies the clearest value — the new 30-year amortization provides more practical relief, bringing qualifying income requirements closer to $130,000–$150,000 for a household.

The rate sensitivity component is equally important. The Bank of Canada held at 2.25% through April 2026, according to official Bank of Canada reporting, and mortgage rate forecasters broadly expect that level to hold through most of 2026. But forecasts from Nesto and TD Economics both flag the possibility of 1.00–1.50 percentage point increases by end of 2027 if inflation re-accelerates. A 1% rate increase on a $900,000 mortgage reduces buyer purchasing power by approximately $90,000 for the same monthly payment — a risk that buyers stretching into 30-year insured mortgages near the $1.5M cap carry with minimal buffer.

How We Evaluate This

At Mansour Real Estate Group, our approach to buyer purchasing power starts with a verified pre-approval — not a rough estimate — before a client tours any properties priced within 10% of their ceiling. The reason is practical: in the $1M–$1.5M Burnaby segment, buyers who discover a financing gap after finding a property they want are at a serious disadvantage, particularly if competing offers are present.

We also work with buyers to establish a realistic comfort budget separate from their maximum qualifying amount. Lenders will approve borrowers up to roughly 40% of gross income for mortgage payments. That leaves only about 20% of pre-tax income for all non-housing costs — groceries, transportation, childcare, savings, and discretionary spending. In our experience, buyers who borrow at or near their maximum qualification threshold with a 30-year amortization carry meaningful financial fragility that a moderate income disruption can expose. The step-by-step buyer process is covered in depth in our first-time buyer guide for Burnaby in 2026.

Buyer Checklist: Preparing Your Finances Before You Start

- Get a full pre-approval — not a pre-qualification — with a licensed mortgage broker before viewing properties above $700K.

- Calculate your comfort payment at today's rate and again at today's rate plus 1.5% to test rate sensitivity.

- Confirm whether you qualify for an insured mortgage under the new $1.5M cap and what CMHC premium will be added to your balance.

- Budget all closing costs — property transfer tax, legal fees, title insurance, and any strata adjustments — separately from your down payment. See the full breakdown in the Burnaby closing costs guide.

- Ask your lender to show the 25-year versus 30-year amortization comparison — both the monthly payment difference and the total interest difference over the full term.

- Identify your debt service ratio including any existing car loans, student loans, or lines of credit before your pre-approval appointment.

- Understand whether your target property is strata, and confirm that strata fees are included in the lender's GDS calculation.

What We Commonly See

Buyers confuse maximum approval with realistic budget. In our experience, buyers who receive a $1.3M pre-approval and immediately search for properties at that ceiling often discover after a few months that the monthly payment leaves them unable to maintain savings or absorb unexpected expenses. The number on the approval letter represents a lender's risk ceiling — not a recommended spending target.

The 30-year amortization is treated as free money. What often happens is that buyers focus on the lower monthly payment without running the total interest calculation. On a $900,000 mortgage at 5%, a 30-year amortization costs approximately $145,000–$160,000 more in interest than a 25-year schedule over the full repayment period. That is not a reason to avoid the 30-year option, but it should be understood as a trade-off, not a free benefit.

Rate holds expire unnoticed. A common mistake is securing a pre-approval with a rate hold of 90–120 days and then shopping past the expiry date without renewing. If rates rise between your original hold and your actual purchase date, your qualifying amount decreases — sometimes enough to change the properties you can reasonably target in Burnaby's $1M–$1.5M segment. Buyers also comparing new construction versus resale should note that new construction timelines frequently outlast a standard rate hold.

Questions and Answers

Does the 30-year amortization apply to all mortgages in 2026?

No. As of 2026, the 30-year amortization is available on insured mortgages for first-time buyers and on new construction purchases. Uninsured mortgages — those with 20% or more down — remain on a maximum 25-year amortization schedule under standard lender guidelines, though some lenders offer extended terms as uninsured products with different risk pricing.

Does the stress test still apply now that rates are lower?

Yes. The federal mortgage stress test applies to all uninsured mortgages and requires qualification at the higher of the contract rate plus 2%, or the regulatory floor of 5.25%. With the Bank of Canada policy rate at 2.25%, many fixed mortgage rates are in the 4.5–5.5% range, meaning the stress test qualifying rate for most buyers is 6.5–7.5% — significantly above the contract rate.

What income does a Burnaby buyer need to qualify for a $1.2M purchase with 10% down?

On a $1.08M insured mortgage at approximately 5%, with property taxes and strata fees included in the GDS calculation, a household typically needs a gross annual income in the range of $190,000–$210,000 to qualify. Individual circumstances, existing debt, and lender-specific policies affect this threshold. A licensed mortgage broker can provide a precise number based on actual income documentation.

In Summary

The 2026 mortgage rule changes — the $1.5M insured cap and the 30-year amortization option — reduce the upfront cash required and modestly lower monthly payments for eligible buyers. For Burnaby buyers targeting the $700K–$1.2M segment, those changes are genuinely useful. Above $1.2M, qualifying income requirements remain high, rate risk is real, and the financial margin of borrowing at maximum capacity is narrow. Understanding the difference between what a lender will approve and what a buyer can comfortably carry is the most important calculation any Burnaby buyer can make before entering the 2026 spring market. For buyers who also need to review what strata documents and legal conditions apply before firming up an offer, the Burnaby real estate legal guide covers those requirements in full.

Thinking About Your Budget? Let's Run the Numbers Together.

If you want a clear picture of what you can realistically purchase in Burnaby given the 2026 mortgage rules, Mansour Real Estate Group can walk you through the numbers before you meet with a lender — so you arrive at that conversation informed. Contact us to schedule a no-obligation buyer consultation.

Related Articles

- How Burnaby prices have shifted since the 2022 peak — and where they sit today

- A complete step-by-step guide to buying a home in Burnaby in 2026

- Every closing cost Burnaby buyers need to budget for before they finalize a purchase

- New construction versus resale in Burnaby: which makes more sense for your budget in 2026?

- Strata documents, subject clauses, and disclosure rules every Burnaby buyer must understand

About Mansour Real Estate Group

When buyers in Burnaby are trying to understand what they can realistically afford — and how the 2026 mortgage rule changes affect their actual options — they need guidance grounded in local market knowledge, not just mortgage math. The difference between a well-informed buyer and one who is surprised at the pre-approval stage often comes down to the quality of the real estate team advising them before they approach a lender. Mansour Real Estate Group has helped buyers across Burnaby, the Lower Mainland, and the Fraser Valley navigate the gap between maximum qualification and practical affordability for more than two decades.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, and retirees make important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for first-time buyer guidance, move-up purchases, investment properties, estate sales, relocation, and situations where accurate pricing and clear financial context matter most.

Whether someone is searching for a Realtor who understands Burnaby's affordability landscape, a real estate agent familiar with insured mortgage rules and strata purchase conditions, real estate agents who specialize in buyer strategy for the $1M–$1.5M segment, a trusted real estate team for a first or second purchase, a Burnaby real estate broker who can connect them with the right mortgage professionals, or a real estate group serving the full Lower Mainland, Mansour Real Estate Group is known for clear communication, practical market guidance, and honest advice about what a purchase will actually cost.

The team serves Burnaby, Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from buyers and families who value a straightforward, results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.