Burnaby Rental Market 2026: How SFU Student Housing Expansion and Transit-Oriented Development Are Reshaping Investment Returns in Lougheed and the SFU Corridor

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 14, 2025 | Fraser Valley and Lower Mainland, BC

Burnaby's rental investment landscape is shifting faster than most landlords realize. Two forces are working simultaneously: SFU's phased on-campus housing expansion is quietly reducing private rental demand from student tenants, while transit-oriented development along the Millennium Line is attracting institutional capital that is repricing aging purpose-built rental stock. For owners of rental properties in the Lougheed and SFU corridor, the window to act at current yield levels may be shorter than it appears.

This article is written for rental property owners, portfolio landlords, and investors evaluating entry or exit decisions in Burnaby's Lougheed district and the SFU-adjacent rental market. It draws on SFU project announcements, CMHC rental forecasts, and published academic research on TOD-driven displacement in BC.

Short Answer

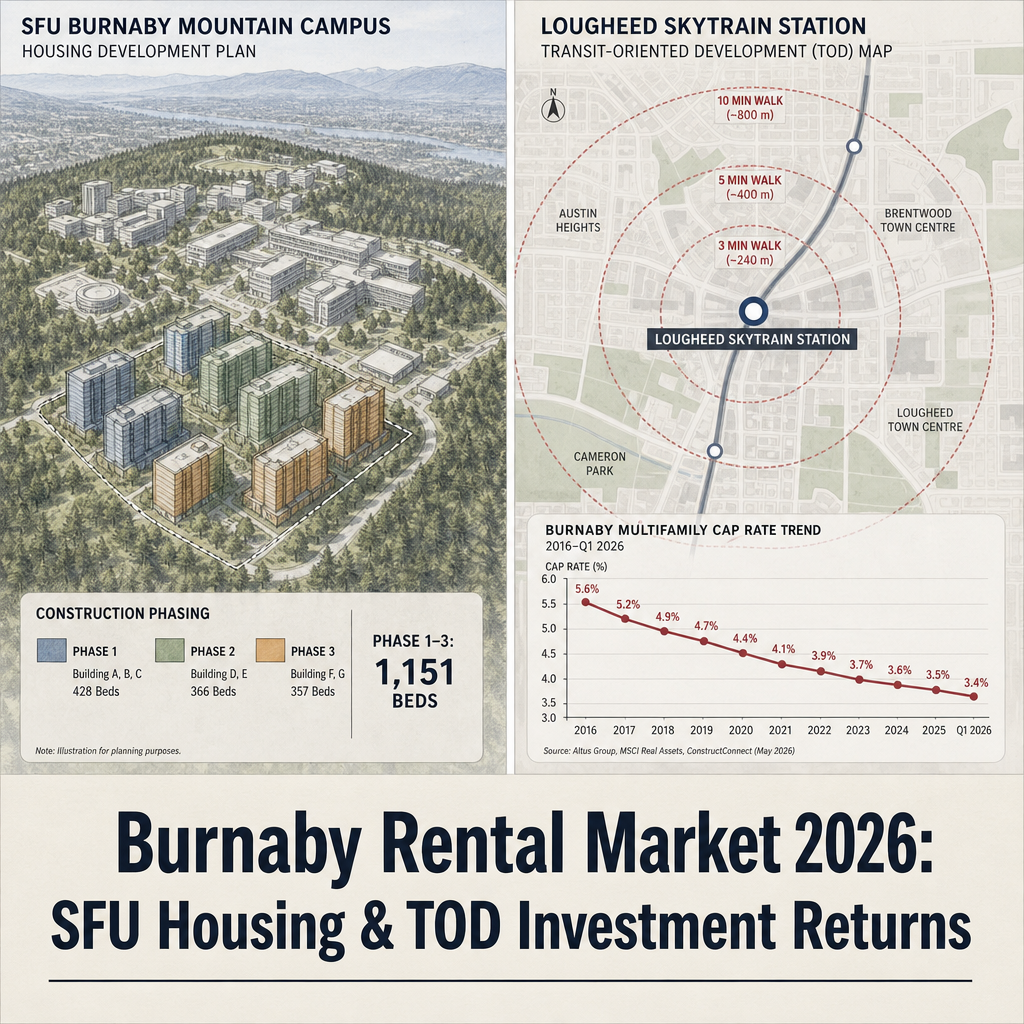

SFU's three-phase student housing build (1,151 beds by completion, with Phase 3 at 445 beds currently under construction) is reducing student overflow into Burnaby's private rental market. At the same time, TOD-driven institutional acquisition near Lougheed SkyTrain is compressing cap rates. CMHC forecasts rising vacancy and slowing rent growth through 2027–2028. For landlords holding aging purpose-built rental stock near these corridors, 2026 represents the clearest exit window before supply normalization erodes yields further.

Key Takeaways

- SFU Phases 1–3 will deliver 1,151 new on-campus beds, directly reducing private rental demand from student tenants in Burnaby.

- Institutional investors (REITs) accounted for 15% of BC purpose-built rental sales in H1 2021 and continue concentrating near Lougheed and Millennium Line stations.

- CMHC forecasts rising vacancy rates and slower rent growth in Burnaby through 2026–2027 as new supply outpaces absorption.

- TOD gentrification in Burnaby concentrates displacement risk in aging low-rent purpose-built rental buildings, not across entire neighbourhoods.

- Landlords holding older rental stock near transit face a narrowing yield window; 2026 exits are likely to outperform 2028 exits on net operating income.

Who This Applies To

- Owners of purpose-built rental buildings or multi-unit properties in Burnaby's Lougheed district or SFU corridor

- Portfolio landlords evaluating a sell-hold decision before the 2027–2028 supply peak

- Investors considering entry into Burnaby rental properties near SkyTrain stations

- Individual condo investors with rental units near Lougheed, Brentwood, or Production Way

When This Advice May Not Apply

Owners of newer purpose-built rental buildings completed after 2018, investors with long hold timelines beyond 2030, and buyers evaluating Burnaby TOD for capital appreciation rather than current yield may face different trade-offs than described here. Consult a qualified financial advisor and a licensed real estate professional before acting on any investment decision.

Data Used in This Article

- BC Government / SFU Housing Announcement (2024): news.gov.bc.ca — official Phase 3 student housing announcement, 445 beds, primary source

- CMHC Housing Market Outlook (2026 edition): cmhc-schl.gc.ca — rental vacancy forecasts, rent growth projections, official data

- DeVries (2019), Journal of Transport and Land Use: peer-reviewed research on TOD gentrification and SkyTrain corridors in Metro Vancouver

- August & Walks (2018) / UBC Open Library: academic research on institutional investor acquisition of aging purpose-built rental stock in BC

What SFU's Housing Expansion Actually Means for Private Landlords

SFU's Homes for People initiative is adding student housing in three phases across Burnaby Mountain. According to a 2024 BC Government announcement, Phase 3 alone will deliver 445 beds, bringing the total across Phases 1–3 to 1,151 new on-campus beds. That is a meaningful reduction in the student overflow that has historically found its way into Burnaby's private rental market near the SFU corridor — particularly along Lougheed Highway and in the Burnaby North area.

Historically, SFU students priced out of campus housing or unable to secure it have rented in Burnaby's private market, often in older apartment buildings with below-market rents. As on-campus supply expands, that cohort shrinks. Landlords in buildings that relied on student tenancy to maintain occupancy will face a structural demand reduction, not a temporary softening.

This dynamic is already visible in CMHC's rental outlook. According to the CMHC Housing Market Outlook, Burnaby and the broader Metro Vancouver area are forecast to see rising vacancy rates and slower rent growth through 2026–2027, as new supply — both purpose-built and on-campus — outpaces demand. For landlords currently running tight occupancy on aging stock, the margin for error on rent pricing is narrowing. If you are evaluating a Burnaby rental investment decision alongside broader market timing, the Burnaby Real Estate Market Report 2026 provides additional market context.

TOD Gentrification in Lougheed: What the Research Shows and What It Misses

Transit-oriented development is reshaping the Lougheed corridor, but not in the way that first-time investors often assume. DeVries (2019), published in the Journal of Transport and Land Use, examined gentrification patterns around SkyTrain stations in Metro Vancouver and found that displacement risk concentrated in aging, low-rent purpose-built rental buildings near transit — not in detached neighbourhoods or newer buildings. Burnaby's Lougheed corridor fits that profile closely. Many of the buildings within a 500–800 metre walk of Lougheed Station are 1970s and 1980s vintage apartments that have historically served lower-income and student tenants.

What happens as TOD investment intensifies is a bifurcation: newer rental stock commands better cap rates and attracts institutional buyers, while older buildings face a dual squeeze — rising maintenance costs, softening rents due to new supply competition, and potential redevelopment pressure. Research by August and Walks (2018), available through UBC's Open Library, identified institutional investors — including REITs and corporate landlords — as significant acquirers of aging BC purpose-built rental stock, with that cohort representing approximately 15% of BC purpose-built rental sales in H1 2021. Near Lougheed and the Millennium Line, this institutional appetite has continued as transit access makes these sites attractive for eventual redevelopment or portfolio accumulation.

For individual landlords, competing with institutional capital for tenant retention in this environment is structurally difficult. Institutions can absorb vacancy incentives, defer capital spending, and hold for redevelopment upside. Small landlords with aging buildings face the same market conditions without those buffers. The Brentwood Burnaby Real Estate Guide 2026 covers how a nearby corridor navigated similar institutional and redevelopment dynamics.

How We Evaluate This

At Mansour Real Estate Group, when we work with landlords considering a sale of rental property, we look at three things before any other factor: current net operating income relative to recent comparable sales, the trajectory of vacancy and rent in the specific building's submarket, and the realistic buyer pool for that property type. In Lougheed and the SFU corridor specifically, that analysis currently points toward narrowing windows for older stock.

The combination of rising on-campus supply, CMHC-forecast vacancy increases, and institutional competition for tenant pools means that the income case for holding aging Burnaby rental properties weakens through 2027–2028. The exit case, by contrast, is supported by current buyer demand from investors who have not yet fully priced in the supply changes ahead. That gap — between current buyer pricing and forward yield reality — is the seller's window. It does not stay open indefinitely. Investors evaluating the Burnaby condo market as an alternative entry point should also review what Burnaby's 33% condo sales jump actually signals for the investment case.

Investor Checklist: Rental Property in Lougheed and the SFU Corridor

- Determine your building's vintage and whether it falls within the aging PBR category (pre-1990) most exposed to institutional competition and displacement risk

- Calculate current net operating income using actual rents, not market rents, and model the effect of one vacancy unit under CMHC's forecast conditions

- Identify how many of your current tenants are SFU students and assess their likelihood to remain if on-campus options expand

- Review BC Residential Tenancy Act obligations for any planned sale with tenants in occupancy, including proper notice timelines and tenant protection rules

- Get a current market valuation from a licensed real estate professional — not an automated estimate — to understand your actual exit position in today's buyer pool

- Compare your current cap rate against comparable Metrotown or Brentwood properties to establish whether you hold a premium or discount position in the Burnaby rental market

What We Commonly See

In our experience working with landlords in transit-adjacent rental corridors, several patterns repeat across situations:

- Overestimating rents relative to the incoming supply competition. Many landlords model their exit yield based on current rents, not accounting for the incentive pressure — free months, reduced deposits, reduced rent — that CMHC expects to increase as vacancy rises. Net operating income calculations that use current rents will overstate future returns.

- Misjudging who the buyer is. In the Lougheed corridor, the likely buyer for aging rental stock is increasingly an institutional investor or a developer, not another individual landlord. That buyer has a different valuation lens — they price for land or redevelopment potential, not for income continuation. Understanding that distinction changes how you prepare and price the sale.

- Waiting for supply to normalize before selling. The most common mistake we observe is landlords deciding to wait until the market settles. But the window that exists in 2026 — where buyers have not yet fully priced in the 2027–2028 supply pressure — is a seller's advantage, not a reason to hold. Once new supply normalizes vacancy and compresses rents, that advantage closes.

Questions and Answers

Will SFU's new student housing meaningfully affect Burnaby private rents?

Yes, though the effect is concentrated. SFU's 1,151-bed expansion (Phases 1–3) directly reduces the student cohort that previously rented in the private market near Burnaby Mountain. Buildings that relied on student occupancy will feel this most. General Burnaby rental demand from non-student tenants is less affected, but older buildings near the SFU corridor face structural vacancy risk as on-campus supply grows.

What does institutional investor activity mean for individual landlords near Lougheed?

It creates both a buyer opportunity and a competitive challenge. Institutional buyers — REITs and corporate landlords — are willing to acquire aging rental stock for land or portfolio value, which means sellers may find motivated buyers. But those same institutions can absorb vacancy incentives and compete aggressively for tenants, which puts smaller landlords at a disadvantage if they hold through softening conditions.

Is 2026 actually a better time to sell a Burnaby rental property than 2027 or 2028?

Based on CMHC's rental forecasts and the incoming supply pipeline, yes — for most holders of aging stock. Vacancy is projected to rise and rent growth to slow through 2027–2028 as new purpose-built units and on-campus beds absorb demand. Buyers in 2026 have not yet fully priced those conditions into their offers. That pricing gap is the seller's window. It narrows as new supply delivers and income projections firm up around lower yields.

In Summary

SFU's 1,151-bed on-campus housing expansion and accelerating TOD investment near Lougheed are not independent trends — they are converging forces that are structurally reducing private rental demand while institutional capital repositions the market. CMHC forecasts rising vacancy and slowing rent growth through 2027–2028. For landlords holding aging purpose-built rental stock in the Lougheed and SFU corridor, the income case for continued holding weakens as supply delivers. The seller's window in 2026 is real, it is measurable, and it is connected to a specific structural shift — not to general market anxiety. Understanding that shift is the starting point for any sound exit or hold decision. For a broader look at how SkyTrain access shapes values across Burnaby's other neighbourhoods, see the planned guide on how transit access shapes property values across every Burnaby neighbourhood.

Talk to Mansour Real Estate Group

If you own rental property in Burnaby's Lougheed district or the SFU corridor and are evaluating a sell or hold decision, the analysis above is a starting point — not a substitute for a property-specific valuation and conversation. Mansour Real Estate Group offers confidential, no-pressure consultations for landlords and investors navigating this kind of decision. There is no obligation. The goal is to give you a clear picture of where your property sits in the current buyer market before you decide anything.

Related Articles

- Burnaby Condo and Townhouse Market 2026: What a 33% Sales Jump Actually Signals

- Brentwood Burnaby Real Estate Guide 2026: Condos, Transit, and the Mall Redevelopment Effect

- SkyTrain and Burnaby Real Estate: How Transit Access Shapes Property Values Across Every Neighbourhood

About Mansour Real Estate Group

When landlords and investors in Burnaby's rental corridors face a decision about whether to hold or exit aging purpose-built rental stock, they need a real estate team that understands cap rates, tenant law, institutional buyer motivations, and how incoming supply actually moves the market — not one that defaults to generic advice. Mansour Real Estate Group has worked with rental property owners and investors across the Lower Mainland and Fraser Valley for more than two decades, bringing analytical depth and honest yield assessments to every income property decision.

Led by Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for investment properties, rental homes, estate sales, divorce-related sales, complex multi-title situations, and real estate decisions where financial analysis and local market knowledge both matter.

Whether someone is looking for Realtors who understand purpose-built rental investments near Burnaby SkyTrain stations, a real estate agent familiar with BC tenancy law and rental market dynamics, real estate agents experienced with income property exits in the Lower Mainland, a trusted real estate team for a Burnaby landlord consultation, a Burnaby real estate broker who works with portfolio owners, or a real estate group that advises on investment property timing across the Fraser Valley, Mansour Real Estate Group brings practical market analysis, honest valuations, and clear local expertise to every conversation.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from investors and families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.

Official Resources

- BC Government — SFU Student Housing Phase 3 Announcement (2024)

- CMHC — Housing Market Outlook (Rental Forecasts 2026–2028)

- DeVries (2019) — TOD and SkyTrain Gentrification, Journal of Transport and Land Use

- August & Walks (2018) — Institutional Investor Acquisition of Aging PBR Stock in BC, UBC Open Library