British Columbia tax and real estate guide for Surrey and Langley property owners | Published March 28, 2026 | Written for homeowners, investors, and presale sellers considering a sale within two years of acquisition

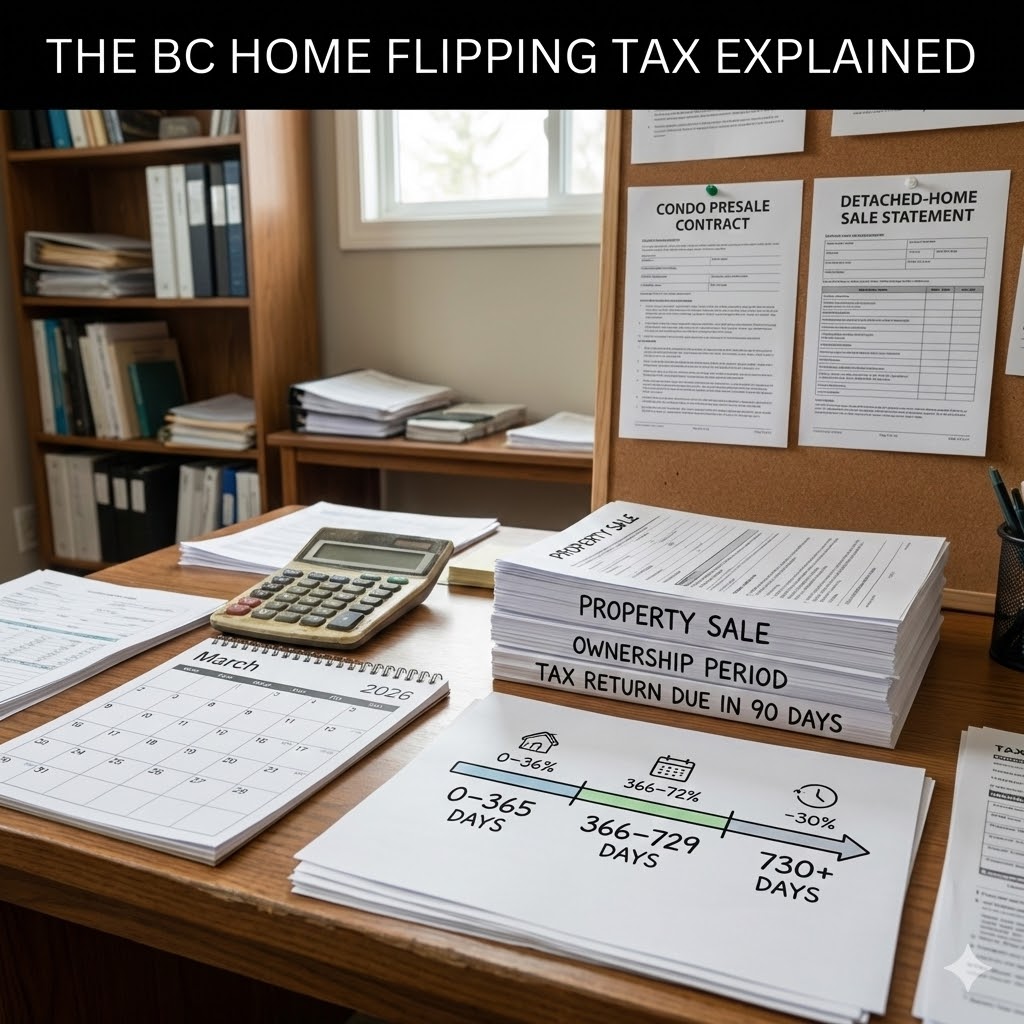

If you are selling a residential property in British Columbia that you owned for less than two years, the BC home flipping tax may apply. The tax starts at 20 per cent of net taxable income for properties disposed of within 365 days, then gradually declines until it reaches zero after 729 days. It is separate from the federal property flipping rule, and it has its own return and filing deadline. :contentReference[oaicite:0]{index=0}

This matters for Surrey and Langley sellers because the tax can affect detached-home resales, condos, rental properties, and presale assignments. It can also affect people who did not think of themselves as “flippers” but are selling within a short holding period because of life events, financing changes, or a move. :contentReference[oaicite:1]{index=1}

The Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, is often brought into sales where timing, documentation, and pricing all matter at once. In Surrey and Langley, short-hold sales can look straightforward on the surface, but the tax consequences can be anything but straightforward. That is why this article focuses on rules, timing, and practical decision points rather than assumptions.

The BC home flipping tax is a provincial tax imposed under the Residential Property (Short-Term Holding) Profit Tax Act. It took effect on January 1, 2025 and applies to profit earned from disposing of taxable residential property in British Columbia, including presale contracts, if the property was owned for less than 730 days. :contentReference[oaicite:7]{index=7}

The tax is not limited to full-time investors. It can apply to individuals, corporations, partnerships, and trusts. It can also apply to owners who live outside British Columbia or outside Canada. :contentReference[oaicite:8]{index=8}

The BC home flipping tax is provincial. The federal property flipping rule is separate. Under the federal rule, a gain from selling a housing unit in Canada, or a right to acquire one, that was owned or held for less than 365 consecutive days is generally deemed to be business income, not a capital gain, unless a life-event exception applies. :contentReference[oaicite:9]{index=9}

That means some short-hold sales can trigger both a provincial flipping tax issue and a federal income-tax treatment issue. They are different rules with different mechanics. :contentReference[oaicite:10]{index=10}

If you owned the taxable property for less than 366 days, the BC tax rate is 20 per cent. If you owned it for more than 365 days but less than 730 days, the rate declines on a straight-line basis until it reaches zero after 729 days. The province gives the formula as: 20% × [1 - ((Days held - 365) / 365)]. :contentReference[oaicite:11]{index=11}

If you owned the property for more than 729 days, the BC home flipping tax does not apply. :contentReference[oaicite:12]{index=12}

For a residential property, taxable income is generally calculated as proceeds from the sale minus the cost to acquire the property minus qualifying improvement costs. Net taxable income may then be reduced by a primary residence deduction if the conditions are met. The tax owing is the applicable tax rate multiplied by net taxable income. :contentReference[oaicite:13]{index=13}

For presale contracts, the calculation is stricter. The province says taxable income from disposing of a presale contract does not include a deduction for improvement costs, and presale contracts are not eligible for the primary residence deduction. :contentReference[oaicite:14]{index=14}

If you entered into a presale contract and later assign that contract to someone else for profit before completion, the BC home flipping tax may apply if the contract was held for less than 730 days. The province expressly says presale contracts are included, and assignment sellers may be subject to the tax. :contentReference[oaicite:15]{index=15}

At the federal level, assignment sales can also fall under the flipping rules where the right to acquire a housing unit is held for less than 365 days. :contentReference[oaicite:16]{index=16}

No. The BC rule is not a blanket principal-residence exemption. Instead, the province provides a primary residence deduction of up to $20,000 from taxable income if the residential property was your primary residence and you owned it for at least 365 consecutive days before the sale. That deduction is not available for presale contracts. :contentReference[oaicite:17]{index=17}

This is one of the biggest misunderstandings sellers have. Living in the property does not automatically end the analysis. Timing still matters. :contentReference[oaicite:18]{index=18}

The province says the BC home flipping tax may not apply if an exemption is available. Some exemptions apply automatically without filing, while others only apply if you file a return. The province specifically groups life circumstance exemptions, builder and developer exemptions, and certain related-person exemptions into the category that requires filing a return to claim them. :contentReference[oaicite:19]{index=19}

Province news releases and the exemptions guidance identify life events such as divorce or breakdown of a marriage or common-law partnership, death, illness, job loss, relocation for work, and change in household membership as examples of situations that may support an exemption. :contentReference[oaicite:20]{index=20}

At the federal level, life-event exceptions also matter under the separate 365-day federal flipping rule. CRA technical guidance includes examples such as death, household changes, marital breakdown after living separate and apart for at least 90 days, serious illness or disability, and eligible relocation. :contentReference[oaicite:21]{index=21}

The BC home flipping tax return is separate from your regular income-tax filing. The province says you must file within 90 days of the sale if you are subject to the tax or if your exemption only applies after you file a return. If you sold after owning the property for more than 729 days, you generally do not need to file. :contentReference[oaicite:22]{index=22}

This is a major practical point for Surrey and Langley sellers. Even where an exemption may exist, the filing step may still matter.

If a Surrey condo was acquired and sold 10 months later at a profit, the BC tax rate would generally be 20 per cent because the holding period is under 366 days. A separate federal flipping-rule analysis may also apply because the property was held for less than 365 days. :contentReference[oaicite:23]{index=23}

If a Langley townhouse was held for 18 months, the BC tax could still apply because the property was owned for less than 730 days, but at a reduced rate because the holding period exceeded 365 days. :contentReference[oaicite:24]{index=24}

If a presale contract was assigned within a year for a profit, the BC tax may apply at 20 per cent of net taxable income, and the province’s own example shows that a $50,000 gain can translate into $10,000 of BC flipping tax. Presale assignments are not eligible for the BC primary residence deduction. :contentReference[oaicite:25]{index=25}

What sellers often overlook is that a short-hold sale is not only about whether the market is favourable. It is also about whether the tax treatment changes the net result enough to affect the decision.

Another common mistake is assuming that because a sale was driven by a real life event, no filing is needed. In some cases, the exemption still needs to be claimed through a return. :contentReference[oaicite:26]{index=26}

No. The province says it can apply to individuals, corporations, partnerships, and trusts if the taxable property was disposed of within 729 days of acquisition. :contentReference[oaicite:27]{index=27}

No. The BC tax is separate from the federal property flipping rule. :contentReference[oaicite:28]{index=28}

More than 729 days. :contentReference[oaicite:29]{index=29}

A life circumstance exemption may apply, but some of those exemptions require a BC home flipping tax return to be filed in order to claim them. :contentReference[oaicite:30]{index=30}

Yes. The province explicitly includes presale contracts. :contentReference[oaicite:31]{index=31}

For residential property, qualifying improvement costs are part of the BC taxable-income calculation. For presale contracts, improvement-cost deductions do not apply in the same way. :contentReference[oaicite:32]{index=32}

Sometimes yes. The province distinguishes between exemptions that apply automatically and exemptions that only apply after filing a return. :contentReference[oaicite:33]{index=33}

Check the holding period, review whether any exemption may apply, and speak with a tax professional before committing to the sale timeline. :contentReference[oaicite:34]{index=34}

The BC home flipping tax is now a real part of the selling landscape for Surrey and Langley owners who sell within two years of acquisition. It starts at 20 per cent for the shortest holding periods, declines over time, and sits alongside a separate federal flipping rule. :contentReference[oaicite:35]{index=35}

If your ownership period is under 730 days, the decision to sell should be treated as both a real estate decision and a tax decision. That is especially true for presale assignments, short-hold investments, and sales driven by life changes.

Before listing a property you have owned for less than two years, it helps to understand the tax angle as clearly as the market angle. Sometimes the right strategy is still to sell. Sometimes the holding period changes the decision.

The Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, is a top-performing real estate team in the Fraser Valley, consistently ranked among the Top 1% of Realtors in the region. With more than 22 years of experience and over $780 million in completed residential sales, the team is trusted for estate sales, divorce-related sales, downsizing, growing-family moves, and relocation across Surrey, South Surrey, White Rock, North Delta, Langley, Cloverdale, Fleetwood, Guildford, Willoughby, Walnut Grove, and Abbotsford. Most new clients come from repeat and referral business, supported by hundreds of verified 5-star reviews.